USDC vs USDT: What's the Difference, and Which Is Safer?

USDC and USDT are cryptocurrencies designed to hold a steady value of one US dollar. USDC is issued by Circle and backed by cash and short-dated US Treasuries, checked every month by Deloitte. USDT is issued by Tether, is more than twice the size, holds gold and bitcoin alongside its Treasuries, and is checked every three months by BDO.

Together they account for roughly 83% of a stablecoin market worth about $303 billion in mid-July 2026.

Key Takeaways

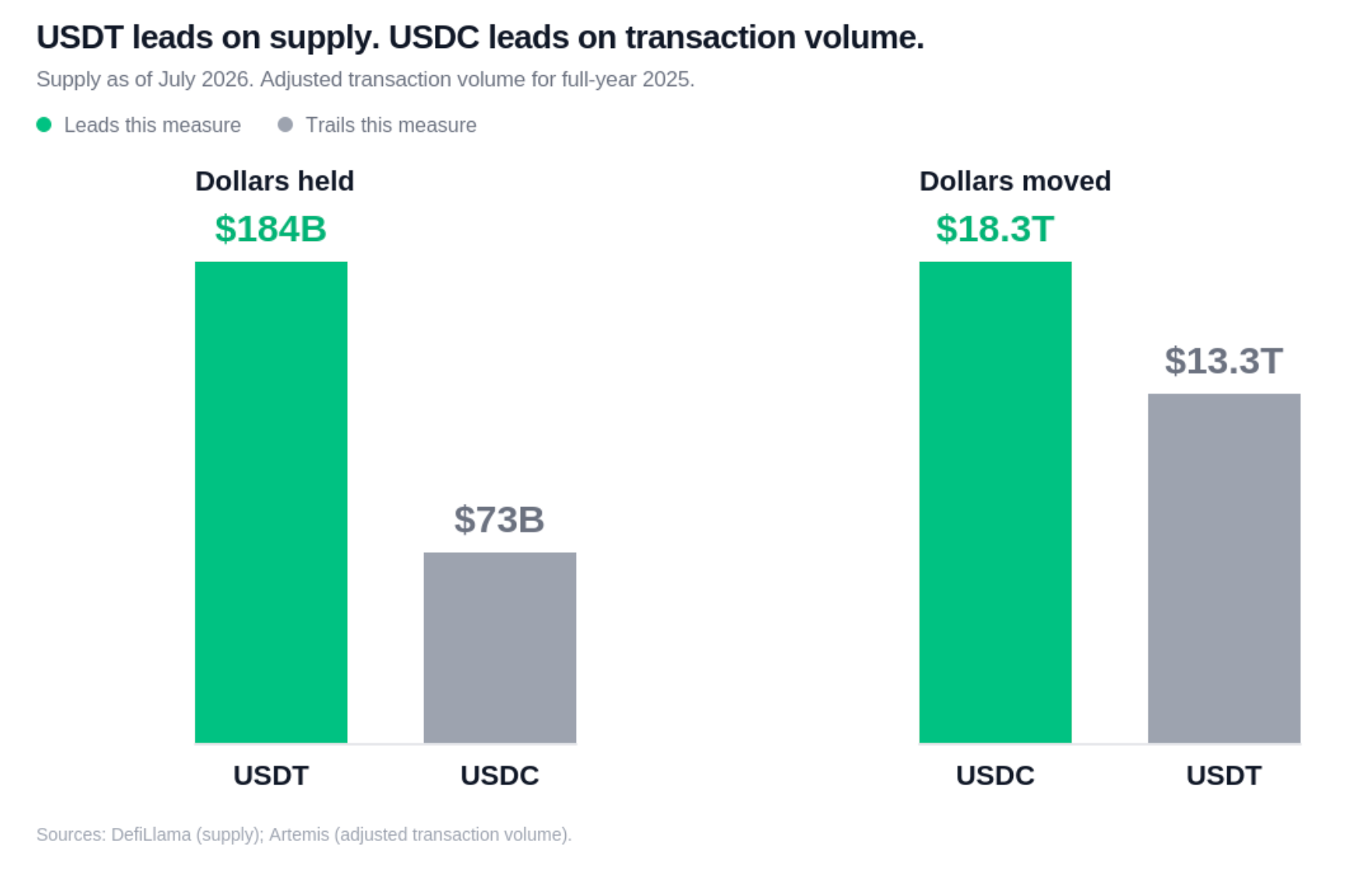

- USDT holds roughly $184 billion in supply against USDC's $73 billion, yet USDC moved $18.3 trillion of transactions in 2025 against USDT's $13.3 trillion.

- Circle publishes a monthly reserve report signed by Deloitte, listing individual securities. Tether publishes a quarterly report signed by BDO, at category level. Neither issuer has published a full audit.

- Both issuers can freeze any wallet, and holding the coins in a personal account does not prevent it. Between 2023 and 2025, Tether blacklisted 7,268 addresses holding $3.29 billion, and Circle blacklisted 372 addresses holding $109 million.

- Neither coin pays interest, and neither is covered by FDIC or SIPC protection.

- Since 1 July 2026, licensed European exchanges can no longer offer USDT to EU users, because Tether did not apply for authorisation under the EU's MiCA rules.

What are stablecoins?

A stablecoin is a cryptocurrency designed to hold a steady value, usually one US dollar. The issuer takes in dollars, holds them in reserve, creates one token for every dollar received, and redeems the token for a dollar on request.

Almost every stablecoin in circulation tracks the dollar, which is why the category matters more outside the United States than inside it. Where a local currency loses value, a dollar-pegged token gives people a way to hold dollars without a US bank account, and saving in dollars is the most common reason people in emerging markets use stablecoins at all.

The six differences between USDC and USDT

| USDC (Circle) | USDT (Tether) | |

|---|---|---|

| How it works | Issued by Circle Internet Financial, a New York company listed on the NYSE, launched September 2018 | Issued by Tether, incorporated in the British Virgin Islands and operating from El Salvador, launched July 2014 |

| What backs it | Cash and short-dated US Treasuries, held mainly in a BlackRock-managed money market fund. No gold, bitcoin, equities or loans | US Treasuries of about $141bn, plus roughly $20bn of physical gold, $7bn of bitcoin, secured loans and other investments |

| Whether it can be frozen | Yes. Circle freezes only on a court order or sanctions listing, and cannot destroy frozen tokens | Yes. Tether freezes proactively with law enforcement, often before a court order, and can burn frozen tokens and reissue them |

| Whether it pays interest | No. The issuer keeps the return on the reserves | No. The issuer keeps the return on the reserves |

| Where it is used | Mostly Ethereum, Base and Solana. Authorised in the EU. Leads on transaction volume | Mostly Tron and Ethereum. Removed from licensed EU exchanges. Dominant in remittance corridors and emerging-market peer-to-peer markets |

| Performance history | One depeg, to $0.87, in March 2023 | Several dips below $0.99 since 2017, the worst around $0.92 |

How do USDC and USDT work?

Both coins are issued by a company that takes dollars in and hands tokens out. Each token is a claim on the reserve behind it, and its value holds at a dollar because the issuer promises to redeem it for one.

Tether launched USDT in July 2014 and now has roughly $184 billion in circulation. Circle launched USDC four years later and now has roughly $73 billion.

Supply measures how many dollars sit still, and transaction volume measures how many dollars move, which is where the ranking reverses. USDC moved $18.3 trillion of transactions in 2025 against USDT's $13.3 trillion, out of a $33 trillion total.

Some of that lead comes from decentralised finance, where the same tokens turn over repeatedly in trading and lending, so the figure measures activity rather than distinct payments. USDT is the larger stock of digital dollars, and USDC is the faster-moving one.

What backs USDC and USDT?

USDC's reserve holds cash and short-dated US Treasuries and nothing else, with the Treasuries sitting in a government money market fund registered with the SEC and managed by BlackRock. Circle publishes a reserve report every month signed by Deloitte, and the fund files its individual holdings daily, so anyone can look up each security in the reserve by name.

Tether's reserve is broader. As of 31 March 2026 it reported $141 billion of US Treasury exposure, about $20 billion of physical gold and about $7 billion of bitcoin, alongside a smaller amount of secured loans, with total assets of $191.8 billion against $183.5 billion of liabilities.

Tether publishes those figures every three months, signed by BDO, giving the total held in each category without naming the securities inside it. A USDC holder can verify the reserve down to the individual bond, while a USDT holder sees category totals and takes the rest on the accountant's word.

Gold and bitcoin also move in price, which means a reserve holding them can fall in value at the moment redemption demand is highest. Tether's answer is that these assets sit inside its excess buffer and that gold performs well in a crisis. Neither issuer publishes a full audit, despite frequent claims otherwise.

Can USDC or USDT be frozen?

Yes. Both tokens carry a freeze function written into the contract, which lets the issuer add any address to a blacklist and stop the tokens in it from moving. Tether can go further and burn frozen tokens, reissuing the same amount to law enforcement or to victims, while Circle can block an address without destroying what sits in it.

Holding either coin in a personal account rather than on an exchange offers no protection, because a personal account guards a user against the platform failing and does nothing about the company that issued the token.

The two issuers use the power very differently. Between 2023 and 2025, Tether blacklisted 7,268 addresses holding $3.29 billion, most of it on Tron, acting on law enforcement requests and its own analysis and often moving before any court order. Circle blacklisted 372 addresses holding $109 million over the same period, and freezes only when a court order or a sanctions listing requires it.

Circle's restraint looks like the safer position for an ordinary holder, and two events in 2026 complicate it. A court order obtained in a sealed case required Circle to freeze sixteen business wallets at once, several belonging to exchanges and payment processors with no apparent connection to the underlying case.

Then in April, attackers drained about $280 million from Drift Protocol on Solana and bridged roughly $230 million of it as USDC to Ethereum through Circle's own cross-chain system. Circle declined to freeze the funds, holding that it can act only on a lawful order. A class action followed in a Massachusetts federal court, and Drift replaced USDC with USDT as its settlement coin.

The two approaches fail in opposite directions. Tether's speed puts anyone wrongly caught in a sweep at risk, and Circle's caution puts anyone whose money has just been stolen at risk.

Do USDC or USDT pay interest?

No. A stablecoin sitting in an account earns nothing, because the issuer earns the return on the reserves behind it and keeps it. Tether reported $1.04 billion in net profit for the first three months of 2026, earned largely on the Treasuries backing USDT, and holders of the coin received none of it.

The GENIUS Act, signed in July 2025, restricts stablecoin issuers from paying interest to holders. The restriction was written to cover issuers without addressing the companies around them, which is why Coinbase can pay USDC holders 3.5% on balances held in its app and call the payment a loyalty reward funded by a share of Circle's reserve income.

A holder can still earn on a stablecoin by lending it to a borrower who pays interest for it, the same arrangement as a bank deposit with the bank removed. That carries its own risks, including software failure and a rate that moves with demand.

Reaching a lending market usually means managing a protocol, a network and a set of rates, and an app can handle those steps instead. Glider is one, where a user holds a stablecoin such as USDC and its Lending earns on the balance while the funds sit idle, with the assets kept in the user's own account and rates shown as an "up to" figure.

Where are USDC and USDT actually used?

The network a person already uses tends to decide which coin they hold. Close to half of USDT's supply sits on Tron, a network with very low transaction costs that became the main rail for remittance corridors and peer-to-peer trading across Asia, Latin America and Africa.

Roughly two-thirds of USDC sits on Ethereum, followed by Solana and Base, where decentralised finance and tokenized assets are concentrated. In much of the world the local exchange and the peer-to-peer counterparty take USDT and some of them take nothing else, so a stronger reserve is of little use to someone who cannot convert the coin where they live.

Europe works the other way. The EU's MiCA rules reached their final deadline on 1 July 2026, and licensed European exchanges can no longer offer USDT to EU users, because Tether never applied for the authorisation the rules require.

Circle did apply, through a French licence covering all 27 member states, so USDC and its euro-pegged sibling EURC remain listed. Holding USDT in a personal account in Europe is still legal.

Has USDC or USDT ever lost its peg?

USDC has broken its peg once. In March 2023, Silicon Valley Bank failed while $3.3 billion of Circle's cash reserves, roughly 8% of the total, sat inside it, and USDC fell to about $0.87 before recovering within roughly 72 hours once US regulators guaranteed the bank's deposits.

Circle responded by moving most of the reserve into the BlackRock-managed fund and limiting how much can sit at any one bank.

USDT has dipped below a dollar more often and less severely, falling to around $0.92 in October 2018 and to about $0.95 in May 2022 during the collapse of Terra. In the two weeks that followed, Tether processed more than $10 billion of redemptions without pausing withdrawals, which remains the strongest evidence that the reserve behind USDT is real and reachable.

Neither coin has failed.

What other stablecoins are there?

The rest of the market is small by comparison. Sky Dollar (USDS) sits near $8 billion, PayPal's PYUSD near $2.8 billion and Ripple's RLUSD near $1.6 billion, all built on the same fiat-backed model.

DAI is backed by other crypto assets locked in software rather than by dollars in a bank, and Ethena's USDe holds its value through a trading strategy rather than a cash reserve.

A smaller stablecoin is harder to sell in quantity and harder to convert into local currency, because there are fewer buyers and sellers at any given moment. That is the main reason the two largest coins keep most of the market.

Which one to hold

For someone holding dollars as savings over months, with access to both, USDC has the more checkable reserve. A monthly report listing individual securities is a real advantage over a quarterly summary that includes gold and bitcoin.

For someone sending money home, paying a supplier or converting into local currency through a peer-to-peer market, the right stablecoin is the one that clears. Across much of Asia, Africa and Latin America that is USDT on Tron.

For someone in the EU, the decision has largely been made already.

Three facts hold for anyone holding either coin: it is not a bank deposit, it earns nothing while it sits still, and it can be frozen by the company that issued it. Those three matter more than the choice between the two.

Frequently asked questions

Is USDC safer than USDT?

USDC has the more transparent reserve, holding only cash and short-dated US Treasuries, with a monthly report from Deloitte listing individual securities. Tether publishes a quarterly report from BDO at category level, and its reserve includes gold and bitcoin. Both coins carry the same freeze risk, and neither has ever failed to redeem.

Are USDC and USDT insured like a bank deposit?

No. Neither coin is covered by FDIC or SIPC protection, and the GENIUS Act states this directly for US payment stablecoins. A stablecoin is a claim on an issuer's reserves rather than a deposit at a bank, so the holder's protection depends on the issuer's structure and on the law.

Can Circle or Tether freeze a wallet a user controls?

Yes. Both tokens contain a freeze function that lets the issuer blacklist any address, and holding the coins in a personal account rather than on an exchange offers no protection against it. Tether can also burn frozen tokens and reissue them, while Circle can block an address without destroying what sits in it.

Can USDT still be held in Europe?

Yes. Holding USDT in a personal account remains legal in the EU. What ended on 1 July 2026 is the ability of MiCA-licensed exchanges to offer it, because Tether did not apply for the e-money authorisation the rules require.

This article is for educational purposes only. It is not financial, investment, legal, or tax advice. Stablecoins carry risk, including the loss of capital, and are not covered by SIPC or FDIC protection. Anyone considering them should do their own research and consider consulting a licensed professional. Figures are dated as of July 2026 and change over time.