What Is Tokenization? A Guide to Turning Assets Into Blockchain Tokens

Tokenization is the process of representing a real-world asset as a digital token on a blockchain, where a regulated firm holds the underlying asset off-chain and the token records a claim on it. A tokenized US Treasury, gold bar, or stock trades and settles on a blockchain while the asset itself remains in custody.

Demand for tokenized dollar assets concentrates outside the United States, in economies where local currencies lose value and access to dollars through local banks is limited. In emerging markets, dollar-denominated tokens function as a savings tool rather than a speculative one. The market has grown quickly: the tokenized real-world asset market held about $27 billion in distributed on-chain value in June 2026, up from roughly $6 billion in early 2025 (rwa.xyz). The stablecoin market, tracked near $300 billion by rwa.xyz that month, reached a record $322 billion in May 2026, larger than the foreign-exchange reserves of 95 countries (CoinDesk).

Key takeaways

- Tokenization issues a real asset, or a claim on it, as a blockchain token; the token is a digital record of ownership while a regulated firm holds the asset off-chain.

- The tokenized real-world asset market held about $27 billion in distributed on-chain value in June 2026, up from roughly $6 billion in early 2025, according to rwa.xyz.

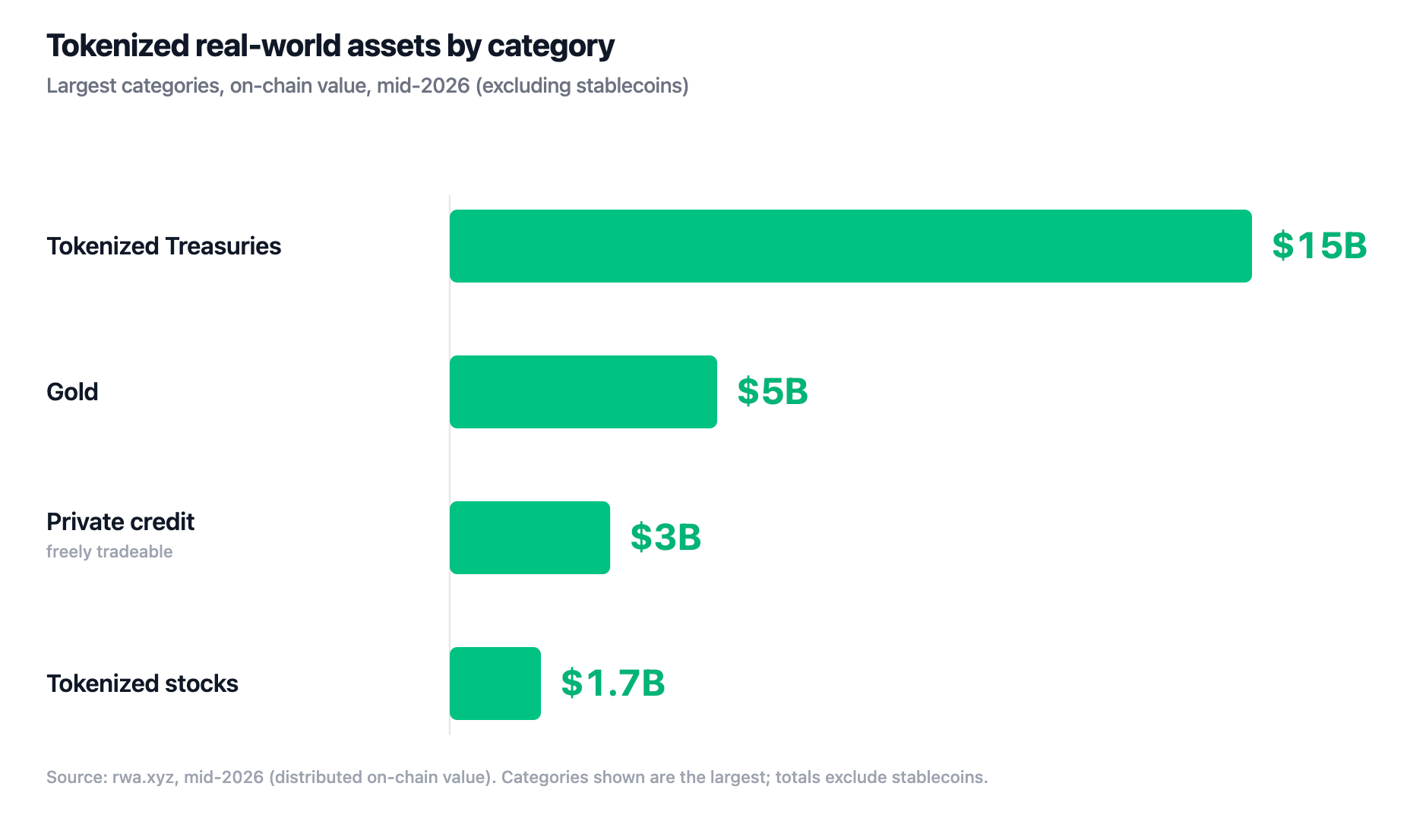

- Tokenized US Treasuries are the largest category, about $15 billion by mid-2026, followed by private credit, gold, and a tokenized-stock segment where Ondo holds over 70% of issuance.

- Tokenized consumer stocks are non-US products by regulatory design; a separate US-market effort led by Nasdaq and the DTCC is different infrastructure.

- Tokenized holdings carry no SIPC or FDIC protection, and third-party tokenized stocks generally confer no voting rights.

What does tokenization mean?

Tokenization means issuing a real asset, or a defined claim on it, as a blockchain token that can be held, transferred, and settled digitally.

How does asset tokenization work?

Asset tokenization follows a defined path from a physical or financial asset to a token held in an account. The token is a digital record of a claim on the asset, and its value depends on the legal and custody arrangements behind it. The asset itself stays with a regulated custodian off-chain.

The steps run in order:

- Structuring. The asset is placed inside a legal wrapper, usually a special purpose vehicle or a registered fund. The token represents a claim on that wrapper.

- Custody. A qualified custodian or licensed broker-dealer holds the real asset, whether Treasury bills, gold bars, or shares.

- Minting. A token is issued for each unit deposited, such as one token per troy ounce of gold or one fund token per share.

- Attestation. A third-party firm periodically verifies the backing. For example, Paxos gold tokens carry a monthly attestation from KPMG.

- Redemption. The holder redeems the token for the asset or for cash, subject to the product's rules.

The outcome of an issuer failure depends on the legal structure. A bankruptcy-remote vehicle legally separates the asset from the issuer's other obligations and offers stronger protection than a contractual promise alone. Because the enforceable rights live off-chain, a token's value in a crisis rests on whether that legal arrangement holds up.

SEC staff described two structural models in a January 2026 statement. In the first, an issuer tokenizes its own security, and the record of ownership simply moves onto a blockchain instead of a conventional database. In the second, a third party wraps a security it did not issue, either by holding the real security in custody and issuing a token that evidences ownership of it, or by issuing a token that tracks the price of a security it does not hold. SEC staff noted that a holder of a third-party token can be exposed to that third party's bankruptcy in a way a direct holder of the underlying security would avoid. The statement reflects the view of SEC staff and carries no legal force.

What can be tokenized?

Almost any asset with clear ownership and a custody path can be tokenized. By mid-2026 at least six categories each held more than $1 billion in on-chain value, and the overall market reached about $27 billion in distributed value in June 2026, excluding stablecoins (rwa.xyz).

There are two important metrics around Tokenized Assets. Distributed value counts tokens that are freely transferable. Represented value counts assets recorded on-chain that may be locked or permissioned, and it runs far higher, near $345 billion in June 2026. Stablecoins, which are dollar-pegged tokens, are tracked separately and stood near $300 billion that month.

The main categories, with dated on-chain figures from rwa.xyz:

| Category | On-chain value (2026) | Notes |

|---|---|---|

| Tokenized US Treasuries | About $15 billion (mid-2026) | Largest and among the fastest-growing; led by Circle USYC, BlackRock BUIDL, and Ondo USDY |

| Private credit | Largest by cumulative origination; a small share is freely tradeable | Higher yields than Treasuries, with real default risk |

| Commodities (gold) | Roughly $4 billion to $6 billion | Tether Gold and PAX Gold hold about 90% of the segment |

| Tokenized stocks | About $1.7 billion distributed (mid-2026) | Non-US by design; Ondo Global Markets holds over 70% |

| Money-market funds | Overlaps Treasuries | Franklin Templeton's BENJI, live since April 2021 |

What are the risks of tokenization?

Tokenization moves an asset onto a blockchain while keeping the risks of the asset and adding new ones. The main tradeoffs are concrete.

- No SIPC or FDIC protection. Tokenized holdings fall outside US brokerage and bank insurance. Recovery after an issuer or custodian failure depends on the legal structure.

- Issuer and custody risk. The token is only as sound as the firm holding the asset and the wrapper around it. A bankruptcy-remote structure protects the holder; a loose promise offers less.

- Smart-contract risk. The token lives in code, and a flaw in that code or its price feed can cause loss.

- No voting rights. Third-party tokenized stocks generally carry no shareholder vote. Ondo added an advisory proxy relay through Broadridge in April 2026, which passes a preference along without binding the outcome.

Tokenized securities in the US market

Tokenization is also being applied to securities inside the regulated US market, which is a separate track from the non-US consumer products described above. In late 2025 and early 2026, the SEC granted a no-action letter for a DTC tokenization pilot and approved a Nasdaq rule allowing tokenized securities to trade on the same order book, with the same rights, as traditional shares. The DTCC, which custodies more than $114 trillion in securities, has scheduled limited production trades and a wider launch during 2026.

These are regulated-market systems that keep traditional ownership rights, dividends, and bankruptcy protections. They are distinct from the non-US tokenized stocks described above and are not available to US persons.

How to access tokenized assets

Tokenized assets can be held without a brokerage account. In supported non-US regions, tokenized Treasuries, gold, and stocks are available from an account funded by card or transfer, with network fees handled in the background.

Glider is one app that offers this. A user funds an account, sets a target mix, and Glider routes and rebalances on a cadence the user chooses. Assets are held in the user's own smart wallet, and the tokenized stocks available are non-US products.

Tokenization changes how an asset is recorded and reached, while the asset itself stays the same. A tokenized Treasury moves with Treasury yields, a tokenized stock moves with its share, and a tokenized gold token moves with the gold price. The value of a tokenized holding depends on the asset behind it and the legal arrangement that connects the two.

Key terms

- Tokenization: issuing a real asset, or a claim on it, as a blockchain token, while a regulated firm holds the asset off-chain.

- Real-world asset (RWA): a traditional asset such as a Treasury, stock, or gold bar represented on a blockchain.

- Custodian: a regulated firm that holds the underlying asset on behalf of token holders.

- Distributed value: the on-chain value of tokens that are freely transferable, as opposed to locked or permissioned.

- Bankruptcy-remote: a legal structure that separates the asset from the issuer's other obligations, protecting holders if the issuer fails.

FAQ

What is tokenization in simple terms?

Tokenization is turning a real asset, or a claim on it, into a digital token on a blockchain. A regulated firm holds the actual asset, such as a Treasury bill or a share, and the token records ownership of that claim. The token can then be held and transferred digitally while the asset stays in custody.

What is an example of tokenization?

A tokenized US Treasury is a common example. A firm holds short-term US government debt in a fund, issues tokens representing shares of that fund, and the token's value tracks the fund while accruing yield. BlackRock's BUIDL, which passed $2.5 billion in 2026, is a tokenized Treasury money-market fund of this kind.

Is tokenization safe?

Tokenization carries the risk of the underlying asset plus new risks of its own, and no SIPC or FDIC protection. Recovery after an issuer or custodian failure depends on the legal structure, so a bankruptcy-remote vehicle protects holders more than a contractual promise. Smart-contract flaws and thin liquidity are additional risks to weigh.

Do tokenized stocks pay dividends?

Most third-party tokenized stocks reinvest the dividend into the position instead of paying cash. A $2 dividend on a $98 token, after a 30% US withholding tax, adds $1.40 of value that buys a fraction of a share, raising the token to about 1.014 shares. These tokens generally carry no voting rights.

How big is the tokenization market?

The tokenized real-world asset market held about $27 billion in distributed on-chain value in June 2026, excluding stablecoins, up from roughly $6 billion in early 2025, according to rwa.xyz. Tokenized US Treasuries are the largest category. Stablecoins are tracked separately and stood near $300 billion.

Disclaimer: This article is for educational purposes only. It is not financial, investment, legal, or tax advice. The tokenized stocks described here are offered to non-US persons only and are not available to US investors. Tokenized assets carry risk, including the loss of capital, and are not covered by SIPC or FDIC protection. Anyone considering them should do their own research and consider consulting a licensed professional. Figures are dated and change over time.