Tokenized Stocks vs CFDs: What's the Difference?

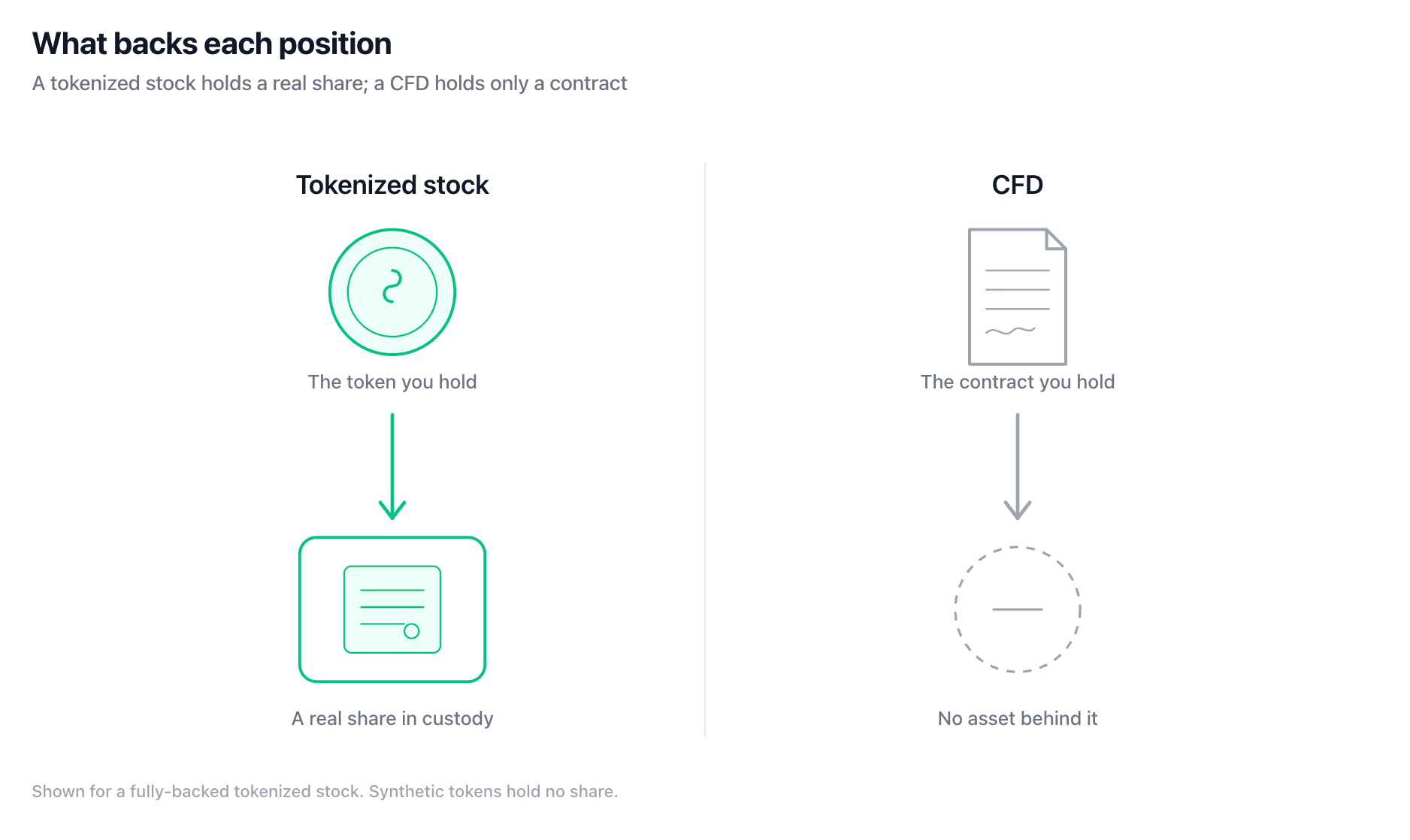

A tokenized stock and a CFD both track a company's share price without making the investor a registered shareholder. The difference is what the investor holds: a tokenized stock is backed by a real share in custody, redeemable for its value, while a CFD is only a contract with a broker that settles the price difference and holds no share.

That difference decides what happens to a position over time, what it costs to hold, and what the holder is left with if the provider fails. Both products are marketed mainly to investors outside the US, so the choice usually comes down to holding period and goal.

Key takeawaysA backed tokenized stock is spot and unleveraged, tied one-to-one to a real share in custody, while a CFD is a leveraged contract with no share behind it.EU and UK rules cap retail CFD leverage on single stocks at 5:1 and require each broker to publish its own loss figure; ESMA's data across EU jurisdictions found between 74% and 89% of retail CFD accounts lose money.A CFD charges a financing fee for every day a position stays open, while a spot tokenized stock has a one-time purchase cost and no daily carry.On the tokenized stocks a non-US investor can buy, dividends are usually reinvested into the token rather than paid as cash, and the holder gets no shareholder vote.

How do tokenized stocks and CFDs work?

A tokenized stock is a blockchain token that tracks a real share, which a regulated firm buys and holds in custody, and it is one type of tokenized real-world asset. A CFD is a contract between an investor and a broker to exchange the difference in a share's price between the moment a position opens and the moment it closes, without any share changing hands.

With a tokenized stock, a licensed firm buys the underlying share, keeps it with a custodian, and issues a token backed one-to-one against it. The token tracks the share price and can be redeemed for its value.

With a CFD, the investor puts up a fraction of the position's value as margin and the broker covers the rest, and that borrowed portion is what creates the leverage. The investor can go long or short, and the profit or loss equals the price change multiplied by the number of units. Because no share is ever bought or delivered, the investor's exposure is to the price alone, never to an asset they hold.

Is there a real share behind a tokenized stock or a CFD?

The clearest difference between the two is whether anything real backs the position. A backed tokenized stock has a share held in custody, and the token carries a claim on that share's value, so the holder owns something that can be redeemed for what it is worth. A CFD has no underlying asset at all, and its value rests entirely on the contract with the broker.

Not every token described as a tokenized stock is backed by a share. Synthetic versions track the price through a smart contract with nothing held behind them, which makes them behave more like a CFD than like a share someone owns. Confirming whether a token is backed or synthetic matters before buying, and US securities regulators treat tokenized securities as securities whichever structure is used.

Are tokenized stocks or CFDs leveraged?

CFDs use leverage as a core feature, while a backed spot tokenized stock uses none. EU and UK product rules cap retail CFD leverage on single equities at 5:1, with a forced close-out at 50% of required margin and negative-balance protection. They also require each broker to publish its own loss figure in a standardized warning, and ESMA's analysis across EU jurisdictions found that between 74% and 89% of retail accounts lose money.

This also makes a CFD risky to hold, because a move against the position can trigger a margin call or an automatic close-out before the trader chooses to exit. A backed tokenized stock has no margin and cannot be liquidated in that way, so the holder only loses money as the share price falls, on top of the separate risks that come from issuer failure, custody problems, and errors in the smart contract.

Some venues do let investors add leverage to tokenized stocks through margin or perpetual futures, and those products behave like a CFD and carry the same amplified risk. A plain backed token bought and held on its own stays spot and unleveraged. CFDs are also effectively unavailable to US retail investors, because the rules push them off-limits rather than banning them outright.

Are tokenized stocks cheaper than CFDs?

Which one costs less depends on how long the position is held. A CFD charges a spread plus an overnight financing fee on the full value of the position, applied every night it stays open and charged at a higher rate once a week to cover the weekend, so the longer a CFD is held the more that financing adds up.

A backed tokenized stock charges a spread and a network fee once, at purchase, and nothing after that for continuing to hold it. A CFD can therefore work out cheaper only for very short trades where the spread is the main cost. For a position held over several weeks or longer, a spot tokenized stock costs far less, because there is no recurring charge for simply keeping it.

Do tokenized stocks and CFDs pay dividends or give voting rights?

On the tokenized stocks a non-US investor can actually buy, dividends are usually reinvested into the token's value rather than paid out as cash, and the holder gets no shareholder vote. The token captures the economic return of the share, while the legal rights stay with the issuer.

A CFD pays no dividend either. When the underlying share goes ex-dividend, the broker applies a cash adjustment that mirrors the price drop, crediting a long position and debiting a short one, and it gives the holder no vote and no claim on the company.

Tokenized stocks vs CFDs: a side-by-side comparison

| Feature | Backed tokenized stock | CFD |

|---|---|---|

| What the holder owns | A token backed one-to-one by a real share in custody, redeemable for its value | A contract with the broker, with no share and no asset behind it |

| Leverage | None; spot and unleveraged | Leveraged; capped at 5:1 on single equities for EU and UK retail, higher offshore |

| Downside mechanics | Loses value only as the price falls; no margin call or forced close-out | Margin calls and automatic close-out at 50% of required margin |

| Cost to hold | One-time spread plus network fee; no daily carry | Spread plus a daily financing fee on the full position value |

| Dividends | Usually reinvested into the token; no cash payout | Cash adjustment mirroring the ex-dividend price move; no real dividend |

| Voting rights | None; the token confers no vote in the underlying company | None; a CFD is a contract, not a share |

| Off-hours liquidity | Trades continuously, but spreads widen when the underlying market is closed | Broker hours, with thin weekend liquidity and wide spreads |

| If the provider fails | Depends on the custody structure; some let holders claim the underlying value, with no guarantee | The holder is an unsecured creditor of the broker |

| Availability | Non-US investors only; US persons screened out | Widely available outside the US; effectively unavailable to US retail |

| Best suited for | Buy-and-hold positions in US equities without a US brokerage | Short-term speculation, shorting, and leveraged directional trades |

When is a tokenized stock better than a CFD?

A CFD suits a short-term trader. It works best for positions held for minutes to days, and its leverage and its ability to go short are what make it useful for speculating, hedging, or betting against a stock. That same leverage is the reason regulators cap it and the reason most retail CFD accounts lose money.

A backed tokenized stock suits a buy-and-hold investor who wants to own something tied to US shares without opening a US brokerage account. It is spot, it carries no daily financing cost, and a real share sits in custody behind the token. An app like Glider is one way to hold spot tokenized US stocks, backed one-to-one and issued through Ondo Finance, for non-US users.

Neither product makes the holder a registered shareholder, and both are ways to track a US share from outside the US financial system. A CFD is built for short, leveraged trades and bleeds financing the longer it stays open, while a backed tokenized stock is built to be held, with a real share in custody behind it and no daily carry. The right one depends on whether the goal is to trade a price for a short while or to hold something backed by a real share for the long run.

Frequently asked questions

Does a CFD give ownership of the stock?

No. A CFD is a contract with a broker to exchange the difference in a share's price between opening and closing a position. No share is bought or delivered, and the holder has no claim on the company. The position exists only as an agreement with the broker.

Are tokenized stocks leveraged?

No. A backed spot tokenized stock is held one-to-one against a real share, with no margin and no risk of forced liquidation. Some venues offer margin or perpetual futures on tokenized stocks, and those products are leveraged and behave like a CFD.

Is a tokenized stock cheaper than a CFD?

It depends on the holding period. A CFD charges a daily financing fee for as long as it stays open, so it only comes out cheaper on very short trades, while a spot tokenized stock has a one-time cost and no daily carry, which makes it cheaper to hold for weeks or longer.

Can US investors buy tokenized stocks?

Generally no. These tokenized stocks are offered under Regulation S to non-US persons, and US persons are screened out when they try to buy. Anyone considering them should first check the rules in their own country.

This article is for general information only and is not investment, financial, legal, or tax advice. The tokenized stocks described here are offered under Regulation S to non-US persons, and availability, rules, and tax treatment vary by country. All investing carries risk, including the possible loss of capital. Readers should do their own research and, where needed, consult a licensed professional before making any decision.