What Is DeFi Lending, and Is It Safe?

DeFi lending, short for decentralized finance lending, is a system that lets people lend and borrow cryptocurrency through software, with no bank or company in the middle. The software runs on a blockchain as self-executing code called smart contracts. Lenders earn interest on crypto that would otherwise sit idle, and borrowers post other crypto as collateral. The rate moves with supply and demand.

The defining feature of DeFi lending is that no company ever takes custody of the funds. The deposited crypto stays in an account the lender controls from start to finish. This shapes both how much a lender can earn and what can go wrong.

Key takeaways

- DeFi lending uses software to connect lenders and borrowers, so the lender keeps control of their assets.

- Interest in DeFi lending is paid by borrowers, who lock up collateral worth more than they borrow.

- Supply rates on major DeFi protocols ran roughly 3% to 10% in mid-2026 and change constantly, differing by network by several points on the same day.

- The main risks are technical, including software bugs and exploits, a pool running out of withdrawable funds, and the deposited token losing value. Aave saw the first two in April 2026.

- DeFi lending has no FDIC or SIPC insurance. Any protection comes from how the protocol is built.

How does DeFi lending work?

DeFi lending works through a lending protocol. A lending protocol is a set of programs called smart contracts that pool deposits and lend them out. A lender adds a cryptocurrency to a pool. A borrower takes a loan from the same pool and posts collateral. The protocol sets the interest rate and enforces the rules automatically.

A lending protocol is software, and the best known are Aave and Compound. It is different from a decentralized exchange such as Uniswap. An exchange swaps one token for another. A lending protocol holds deposits and lends them to borrowers for interest. Each token has its own pool, and the protocol tracks who supplied funds and who owes them.

Every loan is backed by collateral worth more than the amount borrowed. The size of the loan against that collateral is the loan-to-value ratio, or LTV. If the collateral falls too far in value, the protocol sells part of it automatically to repay the loan. A borrower needs no credit check, because the collateral stands behind the loan. Through all of this the deposited funds stay in an account the lender controls and can usually be withdrawn, as long as the pool has funds that are not currently lent out.

Where does the interest come from?

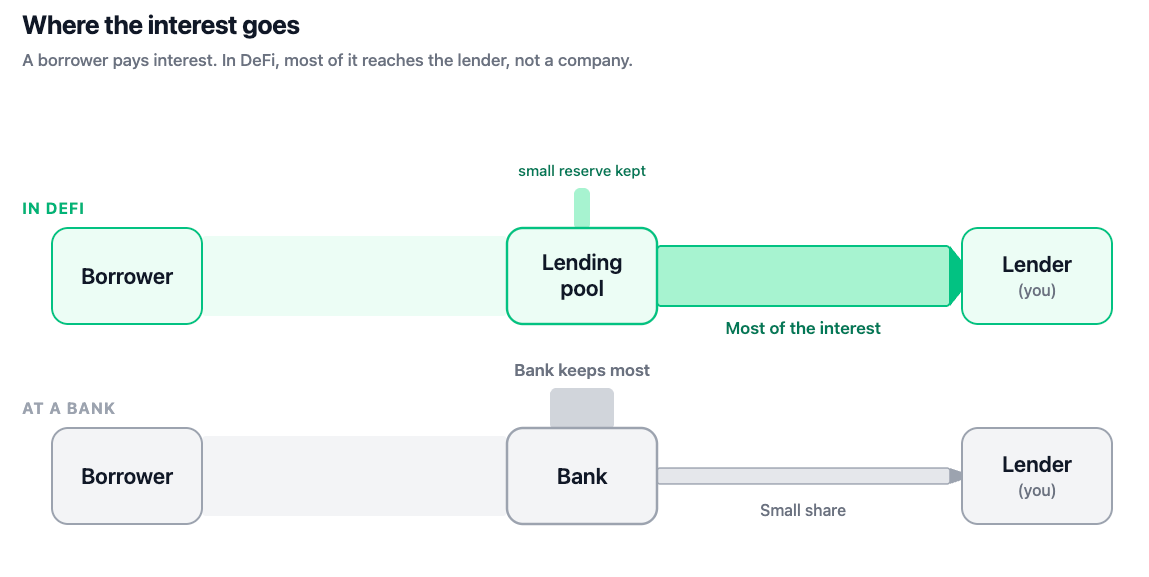

The interest comes from borrowers. Each borrower pays interest on the loan they take. The more of a pool that is borrowed, the more interest there is to share among the lenders who supplied it.

Borrowers use DeFi lending for a few common reasons:

- A trader borrows funds to make a larger trade than their own money allows.

- A holder borrows cash against their crypto so they can spend or invest without selling it.

- An investor borrows a token to sell it now and buy it back later at a lower price.

Every payment a borrower makes becomes part of the lenders' yield.

Illustrative split of interest. Source: general lending mechanic; DefiLlama, 2026

Why do people lend on DeFi protocols?

People lend on DeFi protocols to earn interest on crypto that would otherwise sit idle. The rate is often higher than a traditional savings account. Anyone with a wallet can take part, with no account approval and no geographic limit.

The higher rate comes from the structure of the system. A bank lends out deposits and pays the depositor a small share of what it earns, then keeps the rest. A DeFi protocol passes most of the borrower interest to the lender, so more of it reaches the person who supplied the funds.

How much a lender earns is variable, and the protocol sets the rate automatically. The rate depends on utilization, which is the share of a pool that borrowers have taken out. Rates are not fixed and can change from hour to hour.

The mechanism is simple to follow. When most of a pool is borrowed, the protocol raises the rate. The higher rate draws in more lenders and pushes some borrowers to repay, which keeps the pool from running dry. When little of the pool is borrowed, the rate falls. This is why the same token can pay different rates on different networks at the same time. Demand is higher in some pools than others.

A lender always earns less than a borrower pays. The protocol keeps a portion of the interest as a reserve, and only the borrowed part of the pool earns interest at all. Funds sitting idle in the pool earn nothing until someone borrows them.

In mid-2026, supply rates on established protocols ran roughly 3% to 10% a year, depending on the token, the network, and the day. On one day in June 2026, lending USDC on Aave paid about 3.45% on the Ethereum network and about 9.36% on the higher-demand Arbitrum network. Live trackers such as DefiLlama list current rates.

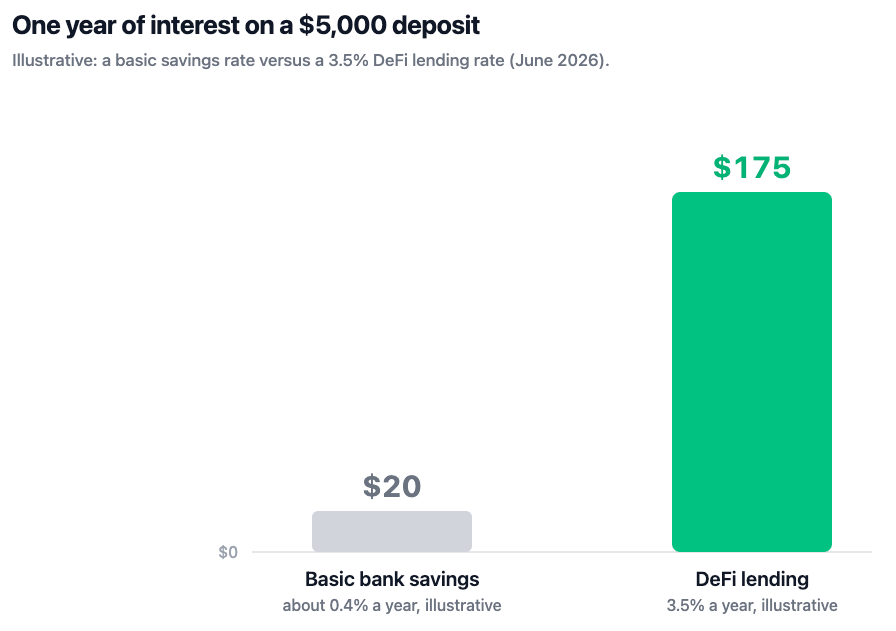

A short example shows the scale. Consider a $5,000 deposit of USDC at a 3.5% rate. That figure is illustrative and close to the live Ethereum rate in June 2026. After one year, the deposit earns about $175. The same amount in a basic bank savings account usually earns less. The $175 holds only if the rate stays the same and the protocol does not fail.

DeFi lending versus a company holding the crypto

The main alternative to DeFi lending is CeFi lending, short for centralized finance. In CeFi, a company takes custody of the funds and lends them out, and the lender depends on that company. In DeFi, software holds the funds and the lender keeps control of the assets in an account they control. The trade is between trusting a company and trusting code.

| CeFi (a company holds the crypto) | DeFi (the lender holds the crypto) | |

|---|---|---|

| Who holds the assets | A company holds the funds on its own books. | The assets stay in an account the lender controls. |

| What the lender trusts | The company stays solvent and honest. | The software works as written and has been audited. |

| Main risk | The company fails, freezes withdrawals, or misuses funds. | A bug or exploit in the software or a connected protocol. |

| Example | Celsius, BlockFi, and Voyager, all collapsed in 2022. | Aave and Compound, two large onchain lending protocols. |

| If it fails | Lenders can become unsecured creditors and recover only part of their money. | An exploit can create bad debt or freeze withdrawals, as Aave saw in April 2026. |

Is DeFi lending safe?

DeFi lending carries several risks that differ from those of a bank. The main one is technical. Two others matter as well: a pool can run out of available funds, and the deposited token can lose value on its own. There is no government insurance.

The clearest technical example came in April 2026. Attackers exploited a service called Kelp DAO and used the proceeds as collateral on Aave. Aave was the largest lending protocol in DeFi at the time. Aave's own software was not the part that was hacked. The protocol was still left with about $196 million in bad debt, and its total value locked, the total amount held in the protocol, fell by about $6.6 billion as lenders pulled their funds. The case shows how a problem in one protocol can spread to another that did nothing wrong.

The same event showed a second risk. A lender can withdraw only the funds a pool is not currently lending out. When borrowing reaches the full size of a pool, a state called 100% utilization, lenders cannot withdraw until borrowers repay or new deposits arrive. During the April 2026 run, several large stablecoin pools on Aave hit 100% utilization, and billions of dollars could not be withdrawn for a time.

A third risk is the deposited token itself. A token can lose value regardless of how the protocol performs. A stablecoin can lose its peg to the dollar, and a more volatile token can fall in price. In either case the deposit can be worth less than before, even when the protocol works exactly as designed.

The custodial alternative has its own record. In 2022, several companies that held customer crypto and paid interest on it collapsed. Celsius was the largest. Its Earn program advertised yields up to 17%, and as high as 18.63% on some assets, and held about $4.2 billion across roughly 600,000 accounts. It froze withdrawals in June 2022 and filed for bankruptcy in July. In January 2023, a court ruled that the crypto in those accounts belonged to the bankruptcy estate, which left those customers as unsecured creditors. DeFi lending removes that specific company from the picture. In exchange, it adds the technical risks above.

No government insurance applies either. In the US, FDIC insurance covers bank deposits up to $250,000, and SIPC covers assets at a failed brokerage. SIPC protects only registered securities, and most cryptocurrency does not qualify. Any protection in DeFi lending comes from the design of the protocol, such as audits and reserve funds, rather than a public guarantee.

How to start with DeFi lending

Using a DeFi protocol directly involves managing a wallet, choosing a network, and tracking rates across protocols. An app can handle those steps and keep the crypto in an account the user controls.

Glider is one such app. A user funds an account, holds a cryptocurrency such as USDC, and its Lending earns interest on that balance while the user decides what to invest in. The network fees and routing are handled in the background, and the assets stay in the user's own account rather than the company's. The rate is whatever the market pays at the time, so it changes with demand.

DeFi lending comes down to two questions. Where does the interest come from, and who holds the funds during the loan. The interest comes from borrowers paying to use the crypto. The funds stay with the lender rather than a company. That structure removes the risk of a custodian failing and adds the technical risks of the software itself. The rate is the easy part to check. The structure behind it is harder to check and matters more.

Key terms

- DeFi (decentralized finance): financial services that run on software on a blockchain rather than through a company.

- DeFi lending: a system for lending and borrowing cryptocurrency through software, where lenders earn interest and borrowers post collateral.

- Lending protocol: the software that pools deposits and lends them to borrowers, such as Aave or Compound.

- Smart contract: self-executing code on a blockchain that carries out rules automatically without a company.

- Collateral: assets a borrower locks up so the lender can be repaid if the borrower does not pay.

- Loan-to-value (LTV): the size of a loan compared with the value of the collateral behind it.

- Liquidation: the automatic sale of a borrower's collateral when its value falls too close to the loan, which repays the lenders.

- Utilization: the share of a lending pool that has been borrowed, which sets the interest rate.

Is DeFi lending safe?

DeFi lending carries real risk. The main risk is technical, such as a bug or an exploit in the software, as happened to Aave in April 2026. A pool can also run out of available funds and block withdrawals, and the deposited token can lose value on its own. There is no FDIC or SIPC insurance, so any protection comes from how the protocol is built.

How does DeFi lending work?

A lender deposits a cryptocurrency into a lending protocol such as Aave or Compound. The protocol lends it to borrowers, who post collateral worth more than the loan. The lender earns interest paid by those borrowers and can usually withdraw the funds, as long as the pool is not fully borrowed. Software handles the lending and the rules, so no company holds the money.

How much can someone earn with DeFi lending?

Rates are variable and change with demand. In mid-2026, supply rates on established protocols ran roughly 3% to 10% a year. They differ by network, sometimes by several points on the same day. A quoted figure only describes that moment and can change within hours.

What is the difference between DeFi and CeFi lending?

In CeFi lending, a company takes custody of the funds and lends them out, so the lender depends on that company. In DeFi lending, software holds the funds and the lender keeps control of the assets. CeFi adds the risk of the company failing. DeFi adds the risk of the software failing.

What is LTV in DeFi lending?

LTV stands for loan-to-value. It measures the size of a loan against the value of the collateral behind it. A borrower who locks up $1,000 of collateral and borrows $500 has an LTV of 50%. A lower LTV leaves a larger buffer. If the collateral falls too far in value, the protocol sells part of it to repay the loan.

Disclaimer: This guide is for educational purposes only and is not financial advice or a recommendation to buy, sell, or lend any asset. Rates mentioned are variable, shown for illustration, and change constantly. Always do your own research.