What Is APY in Crypto? How to Read the Number Behind a Yield

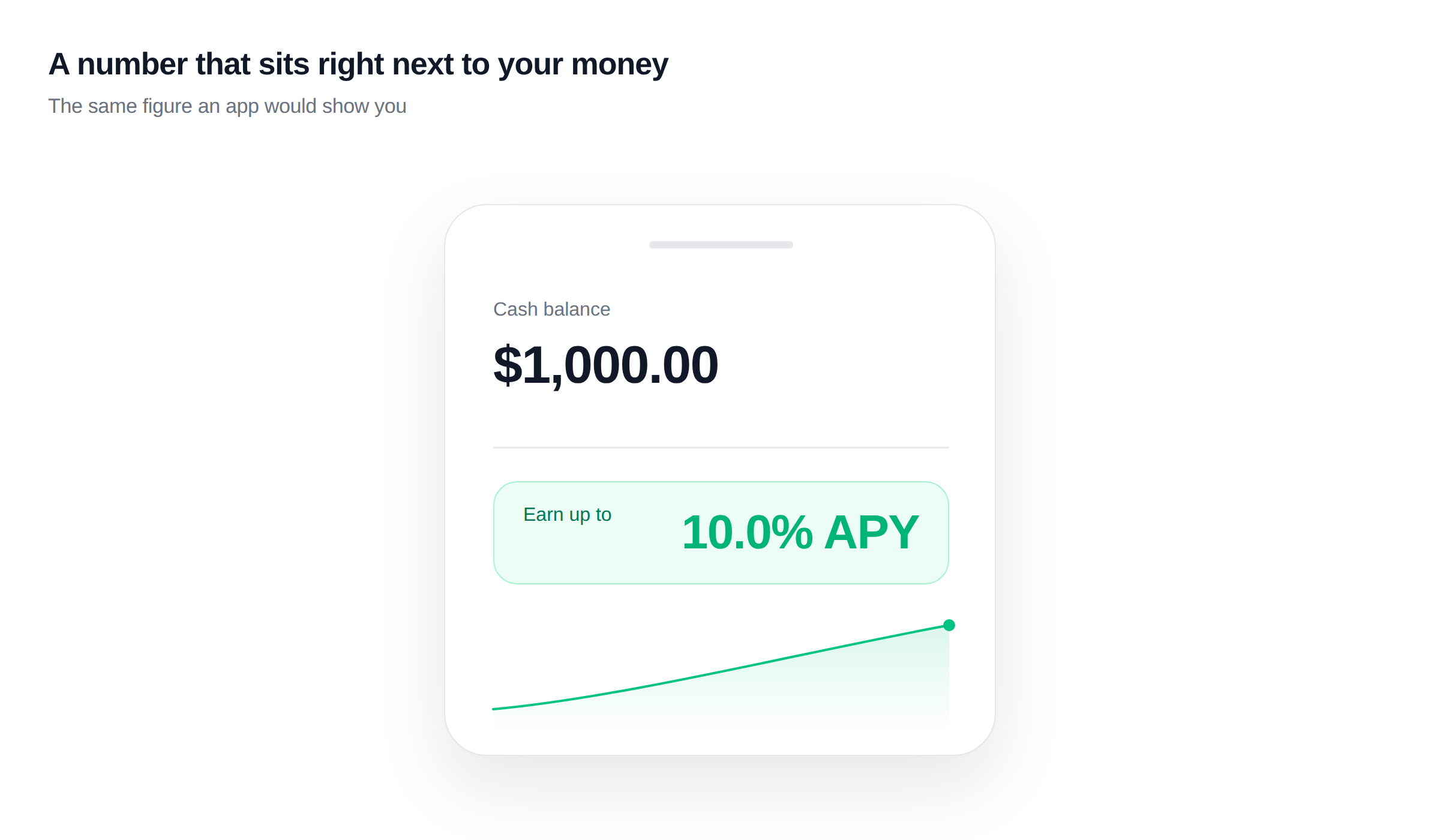

You open a crypto app, and it offers to pay you 10% over the year if you deposit your assets into the app. That is far more than a bank has paid on cash in a long time, and the figure sits right there next to your money, easy to read and easy to trust. A number like that, an APY, hides a fair amount underneath it. Before you act on a high APY in crypto, you want to understand what it actually means and where a return that size is coming from, because that is what separates a real offer from one that only looks good.

What APY in crypto actually is

You earn yield on your assets when you deposit them somewhere and let them be put to work. It's the same basic idea as the interest a bank pays you: you leave your money, it gets used, and you get paid a percentage in return. If you deposit $1,000 and earn $50 over some period, that is a 5% yield on what you put in. APY, short for annual percentage yield, is that same percentage expressed as a yearly figure, so you can line up offers against each other no matter what stretch of time each one is quoted over.

What stands out about APY in crypto is the size of it. A rate that would be unusual at a bank turns up routinely on a crypto app, and that gap is the first clue to where the return is actually coming from.

Where the return comes from

A bank pays you interest because it takes your deposit, lends it out at a higher rate, and keeps most of the difference. What you see is whatever is left after the bank has taken its cut. A crypto rate is usually higher for a plain reason: your money is still being lent to people who pay to borrow it, but there's no bank in the middle keeping most of the spread, so more of that lending return reaches you. Our piece on stablecoin yield goes deeper on exactly where it originates.

That is also why the source matters as much as the number. The return isn't free and it isn't invented; it's paid by real borrowing demand, or by whatever a platform is doing with your money.

APY vs APR

This is the pair that confuses people most, because the two sound almost identical. The difference is compounding.

APR is the simpler one. It just adds the rate up across the year, with no compounding counted in. APY takes that same rate and includes the compounding effect on top, where you start earning on the returns your money has already made, not only on what you first put in. For the same underlying rate, that makes the APY the larger number whenever the interest compounds more than once a year, which in crypto it almost always does. (If it only compounded once a year, the two would be equal.)

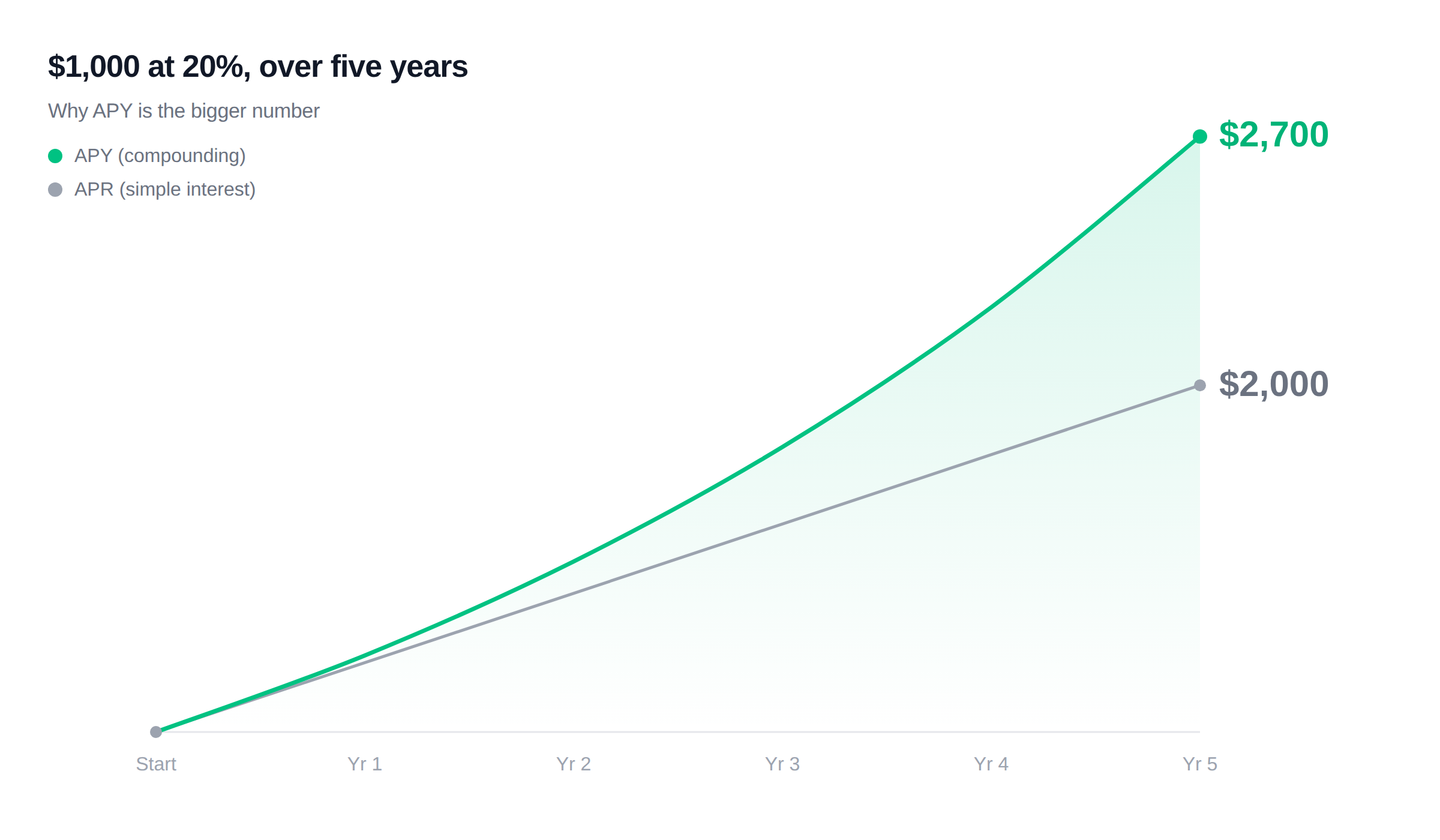

A worked example shows the gap. Put in $1,000 at a stated 20%:

- Quoted as APR, with the interest paid out to you and not reinvested, you collect a flat $200 a year. That is $1,200 after one year and $2,000 after five.

- Quoted as APY, with the same 20% compounding daily and left in to keep earning, the rate works out to about 22.1%. That is roughly $1,221 after one year, and about $2,700 after five.

Two things drive that gap: how often the return compounds, and whether you leave it in to keep earning. The label tells you whether the headline number already includes compounding. APR doesn't, APY does, and that's why the same return can be made to look bigger just by quoting the APY.

How to read an APY before you trust it

Knowing what the number means is very important, but reading it in practice comes down to three questions, none of them complicated.

- Is it APY or APR? The same offer looks better under whichever label is larger, so check which one you're being shown before you compare it to anything else.

- Is the rate fixed or variable? This is the one that catches the most people. A 20% rate that holds all year is a completely different thing from a 20% rate that resets to, say, 4% two weeks in once a promotion ends. Hold the high rate for fourteen days and the low one for the rest of the year and your actual return lands near 4.6%, not 20%. The headline described a fortnight, not your year. A variable rate is a promise with an expiry date.

- Where is the return coming from, and can it last? A rate is only as reliable as whatever pays it. One sitting at a sensible level usually has an ordinary source behind it; one far above everything else is worth understanding before you commit, not a free lunch nobody else spotted. And the rate is only half the picture: a real return can still sit on top of a platform or a coin that carries its own risk, and the APY says nothing about that.

💡 A high APY is a question worth investigating, not an answer you can take at face value.

Letting an app handle it

The simplest version of all this is not having to track the number yourself. You hold a fully reserved stablecoin like USDC, a digital dollar designed to stay worth a dollar, and keep it somewhere that captures the lending return on your behalf, instead of comparing rates and moving money between platforms by hand.

An app like Glider works this way. You fund an account, hold a stablecoin like USDC, and it earns through Lending without you managing rates or chasing a platform around. The rate still depends on the same things every rate in this piece depends on, so none of the three questions above stop mattering. You're just no longer the one doing the legwork on each of them.

A big APY is the easiest thing in the world to put on a screen, and on its own it tells you almost nothing about whether you'll ever see it. Once you can read it, knowing what the number measures, where the return behind it comes from, and whether it's built to last, a large figure stops being something you take on faith and becomes something you can simply check.

FAQ

What does APY mean in crypto?

APY stands for annual percentage yield, the percentage you earn on a deposit over a year once compounding is counted in. In crypto it works the same way it does at a bank, but the rates tend to be higher because your money is lent out without a bank in the middle keeping most of the spread.

Is a high APY in crypto good?

Not on its own. A high APY is only as good as what sits behind it, so it matters whether the rate is fixed or variable, where the return comes from, and whether it can last. A number far above everything else around it is usually a reason to look closer, not a free win.

What is a 7-day APY in crypto?

A 7-day APY takes the return earned over the past seven days and projects it across a full year. It's a useful snapshot of a variable rate right now, but because it rests on a single recent week, it moves around and won't necessarily match what you actually earn over twelve months.

Is crypto APY fixed or variable?

Most crypto APYs are variable, meaning the rate rises and falls as borrowing demand and market conditions change. Some products also advertise a high promotional rate that drops after a short window, so it's worth checking whether a quoted rate is one you keep or one that resets.