What is Tokenized Private Credit?

Tokenized private credit is a blockchain token that represents a claim on a private loan, a loan made to a company by a lender other than a bank. The lender arranges and manages the loan off-chain, and the token carries the right to its interest and repayment. It pays more than a government bond because it carries more risk.

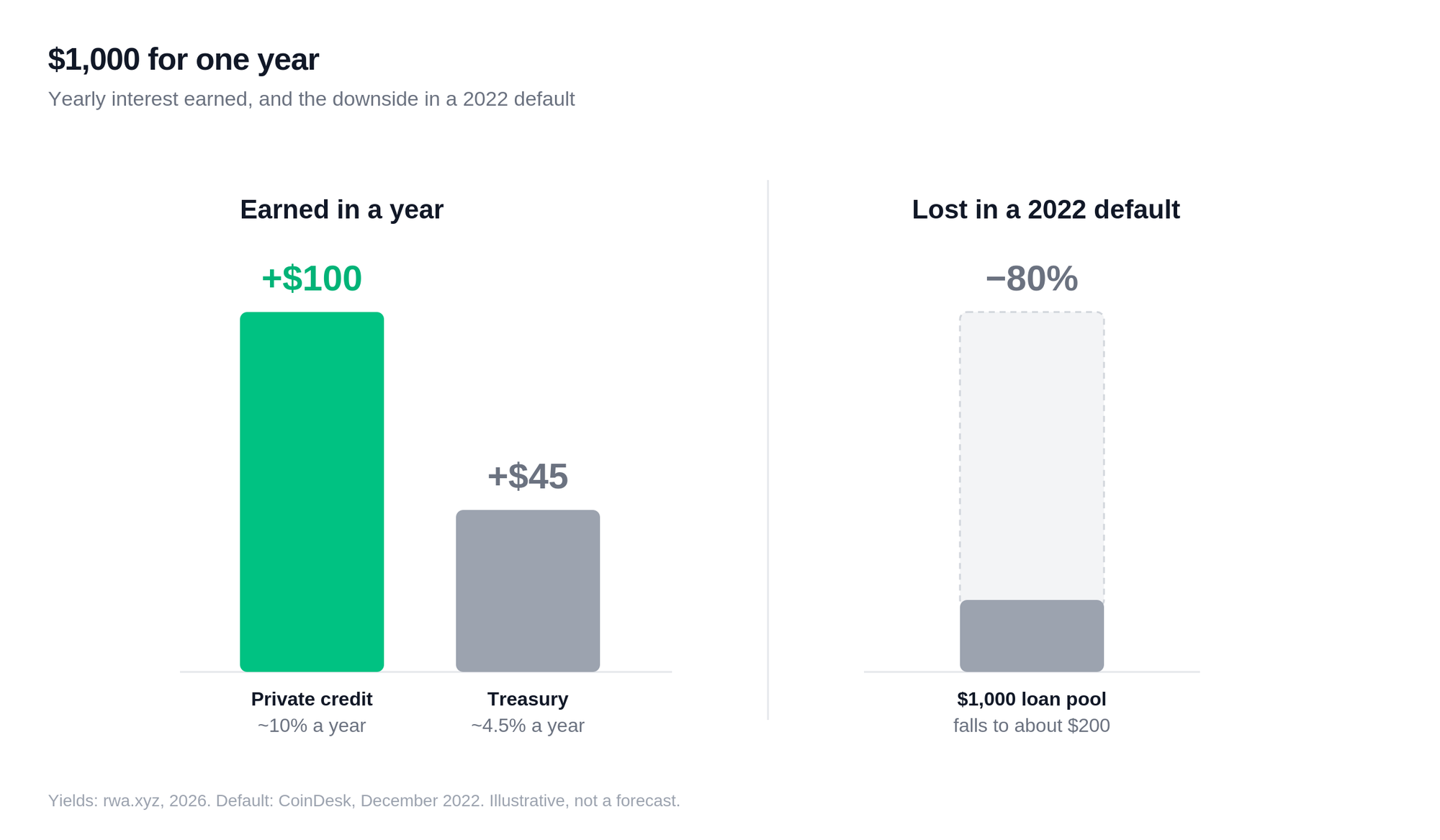

Investors hold it for the higher rate. Tokenized private credit paid an average of about 10% in 2026, more than double what a tokenized US Treasury pays. That extra return carries real risk: in one 2022 default, investors in the worst-hit lending pool lost about 80% of their money.

Key takeaways

- Tokenized private credit represents loans to companies, made by non-bank lenders, as tokens that pay the loan's interest to the holder.

- Borrower yields run about 8% to 12%, averaging near 10%, well above tokenized US Treasuries at roughly 4% to 5%.

- Active tokenized private-credit loans passed $19 billion by late 2025 and have grown since, but only around 12% is held in a form an investor can freely trade.

- Most tokenized private credit is limited to institutions and wealthy investors, with a small set of products open to non-US retail investors who pass an identity check.

- In December 2022, one borrower defaulted on $36 million on the lending platform Maple, and investors in the worst-hit pool lost about 80% of their remaining money.

What is private credit?

Private credit is a loan to a company from a non-bank lender, such as an investment fund or a specialty finance firm, arranged privately instead of through a bank or the public bond market.

The loans are not listed on an exchange, and the fund that makes one usually holds it until the borrower repays. Private credit covers direct loans to mid-sized companies, loans backed by real estate, and financing against unpaid invoices. It grew into a large asset class after the 2008 financial crisis, when tighter rules pushed banks out of this kind of lending and funds stepped in. The traditional private credit market is about $1.6 trillion measured as direct lending, and roughly $3 trillion counting all private debt. Funds lend this way because the rate runs higher than government or investment-grade corporate debt.

What is tokenization?

Tokenization means creating a digital version of an asset on a blockchain, a public ledger anyone can read, so a claim on it can be held and moved without the usual paperwork.

The asset itself does not change. A regulated firm still holds it, and the token records who has a claim on it. Stocks, bonds, gold, and Treasuries are already tokenized this way, and private credit is one more asset that fits the model.

What is tokenized private credit?

Tokenized private credit combines the two: a private loan, with the claim on it issued as a blockchain token. The loan is originated and serviced the same way as any private loan, and the blockchain adds a record of who holds the claim.

The token is almost always a financial security, and recording it on a blockchain does not change how the law treats it. Issuers sell it under exemptions that limit who can buy, so access depends as much on regulation as on the technology.

How does tokenized private credit work?

A lender makes a loan to a company and checks that it can repay, all off-chain. A separate legal entity is set up to hold the loan, which gives token holders a claim if the borrower fails. The issuer then creates tokens that represent a share of the loan, and investors buy them with dollars or stablecoins after passing an identity check. A stablecoin is a cryptocurrency designed to hold a steady value, usually one US dollar. As the borrower pays interest, that money reaches token holders, either as payouts or as a rising token value. Some products let holders redeem on set dates, while others are held until the loan matures.

How big is the tokenized private credit market?

Tokenized private credit is one of the largest categories of tokenized real-world assets by loan value, though most of that value is a record rather than something an investor can trade.

Active tokenized private-credit loans passed $19 billion by late 2025 and have grown since. Only around 12% of those loans are held in a form that can be freely moved, under $3 billion in total. The rest is an onchain record of loans an ordinary investor cannot transfer. Figure, the largest issuer, accounts for roughly three-quarters of tokenized private credit by loan value, and its home-equity token is used only as an onchain record rather than something investors can trade. The main issuers of tradeable tokens include Maple, Goldfinch, and Centrifuge, while large managers such as Apollo, Hamilton Lane, and KKR have brought private-credit funds onchain for institutions. The buyers are mostly institutions, credit funds, and wealthy investors, with a smaller share of products open to non-US retail.

| Measure | Value |

|---|---|

| Active tokenized private-credit loans | More than $19 billion by late 2025, growing since |

| Held in a freely tradeable form | About 12%, under $3 billion |

| Typical borrower yield | About 8% to 12% |

| Traditional private credit market | About $1.6 trillion to $3 trillion |

Source: rwa.xyz.

How much does tokenized private credit yield?

Tokenized private credit paid an average of about 10% in 2026, higher than a tokenized Treasury because it lends to a single company that can miss a payment.

Take $1,000 held for one year. At the tokenized private-credit average of about 10%, it earns about $100 in interest. The same $1,000 in a tokenized US Treasury at about 4.5% earns about $45. The private-credit position pays roughly $55 more, a little over double. The risk shows on the other side: in the 2022 Maple default, holders in the worst-hit pool lost about 80% of their money, which would have cut a $1,000 position toward $200.

What are the risks of tokenized private credit?

The main risks are that a borrower defaults, that the loan is hard to sell before it matures, and that the software or the firm holding the loan fails. Tokenizing a loan removes none of them.

Private credit lends to a single company, and a company can stop paying. In December 2022, the crypto firm Orthogonal Trading defaulted on $36 million on Maple, and investors in the worst pool lost about 80% of their remaining capital. Private loans are also hard to exit early, since tokenizing one does not create a buyer. Private credit is valued using the lender's own estimates rather than a live price, so trouble can surface late. These products work like onchain DeFi lending for institutions, and the same failures apply.

How to invest in tokenized private credit

Reaching tokenized private credit as a non-US retail investor means holding an account that supports it, funding it with stablecoins, and passing an identity check. The large institutional funds stay gated, so the realistic options are the few products open to retail.

An app like Glider is one way to hold tokenized private credit without a brokerage account. Through its Nest Vaults, built with Plume and Nest, a user can hold nALPHA, a vault that invests in tokenized private-credit strategies. The assets sit in the user's own account, and Glider covers the network fees and routing. Yields are variable and shown as an "up to" figure, never a promise, and access depends on the country.

Tokenized private credit pays more than a government bond because it lends to companies that can miss a payment. The token makes the claim easier to hold and, for part of the market, easier to move. Whether it pays off still depends on whether the borrowers repay.

FAQ

Is tokenized private credit safe?

Tokenized private credit carries real risk and is not a safe asset like a government bond. It lends to individual companies that can default, the loans are hard to sell early, and there is software and custody risk on top. In a 2022 default on Maple, holders in the worst pool lost about 80% of their remaining capital.

Can retail investors buy tokenized private credit?

Most tokenized private credit is limited to institutions and wealthy investors who meet income or wealth thresholds. A small set of products is open to non-US retail investors who pass an identity check, such as Maple's syrupUSDC, which has no minimum. Access still depends on the buyer's country.

What yield does tokenized private credit pay?

Borrower yields on tokenized private credit run about 8% to 12%, averaging near 10%. Rates are variable and depend on the loans underneath. They run higher than tokenized US Treasuries, which recently paid around 4% to 5%.

How is tokenized private credit different from tokenized Treasuries?

A tokenized Treasury represents short-term US government debt and carries almost no default risk, paying about 4% to 5%. Tokenized private credit represents loans to individual companies, pays more, near 10%, and carries the risk that a borrower does not repay. The higher rate is the return for taking that risk.

This article is for educational purposes only and is not financial, investment, legal, or tax advice. Tokenized assets carry risk, including the loss of capital. Anyone considering them should do their own research and consider consulting a licensed professional.