What Are Real-World Assets (RWAs) and How Do They Work?

Real-world assets, or RWAs, have grown up fast. The value of these assets held on blockchains has gone from under $3 billion in mid-2024 to around $34 billion in mid-2026, a tenfold jump in under two years, and that is before counting stablecoins. Big names like BlackRock and Franklin Templeton have launched tokenized funds of their own.

Several things have converged to drive this: clearer rules in the US, more mature onchain infrastructure for institutions, and a wave of banks and asset managers shifting from blockchain pilots to live products. Most forecasts expect the market to keep climbing from here, with several running into the trillions of dollars by 2030.

What are real-world assets?

A real-world asset is something that has value in the ordinary financial world, such as a government bond, a share in a company, an ounce of gold, or a dollar. An RWA is one of those assets issued as a token on a blockchain.

To understand what that token is, it helps to know what a blockchain token does. A blockchain is a shared record that many computers keep in sync. A token is an entry on that record showing who holds what, and it can move from one holder to another by updating that shared record. Putting a real asset onchain means issuing a token that stands in for it, so ownership can be tracked and transferred there instead of inside one firm's private books.

Behind every token is a real asset held somewhere in the world. A regulated firm holds the real bonds or the real gold and issues tokens backed by what it holds, with each token a claim on the underlying asset. Once the token exists, it can be held in an account, sent, or sold at any time, including weekends, often without routing through a brokerage in a particular country.

What can be tokenized

The list of items that are getting tokenized is very broad:

- Government debt: Around $15 billion exists onchain, mostly tokenized US Treasuries.

- Private credit: Corporate loans and lending products from issuers like Maple and Figure. Counts swing from about $5 billion freely transferable to $18 billion-plus, since much of it sits on restricted chains.

- Gold: About $5 billion, almost entirely gold (PAXG and Tether's XAUT). Silver and all other commodity tokens combined make up only around $57 million.

- Stocks: Around $1.5 billion in tokenized shares, which usually track the share price but come without voting rights.

- Funds: A few billion dollars, larger than stocks, mostly money-market funds.

- Dollars, as stablecoins: By far the biggest at around $300 billion, led by USDT and USDC and usually counted separately. They settled transactions worth roughly $33 trillion in 2025, on par with the major card networks.

Whether the token gives you just a claim on the price, or also the dividends and interest, depends on the asset and how the issuer set it up.

Why tokenize real-world assets?

Putting an asset onchain is meant to fix a few long-standing frictions in traditional finance:

- Fractional ownership: Customers can buy a part of something expensive, like a piece of land or a bar of gold, instead of the whole thing, which lowers the entry price for ordinary investors.

- Enhanced liquidity: Assets that are normally slow and hard to sell, such as real estate, can trade on digital markets that run around the clock.

- Global access: Anyone with an internet connection can hold assets that once required a local broker or bank, subject to the rules where they live.

- Transparency: On public chains, ownership and transfers sit on a shared ledger that anyone can verify.

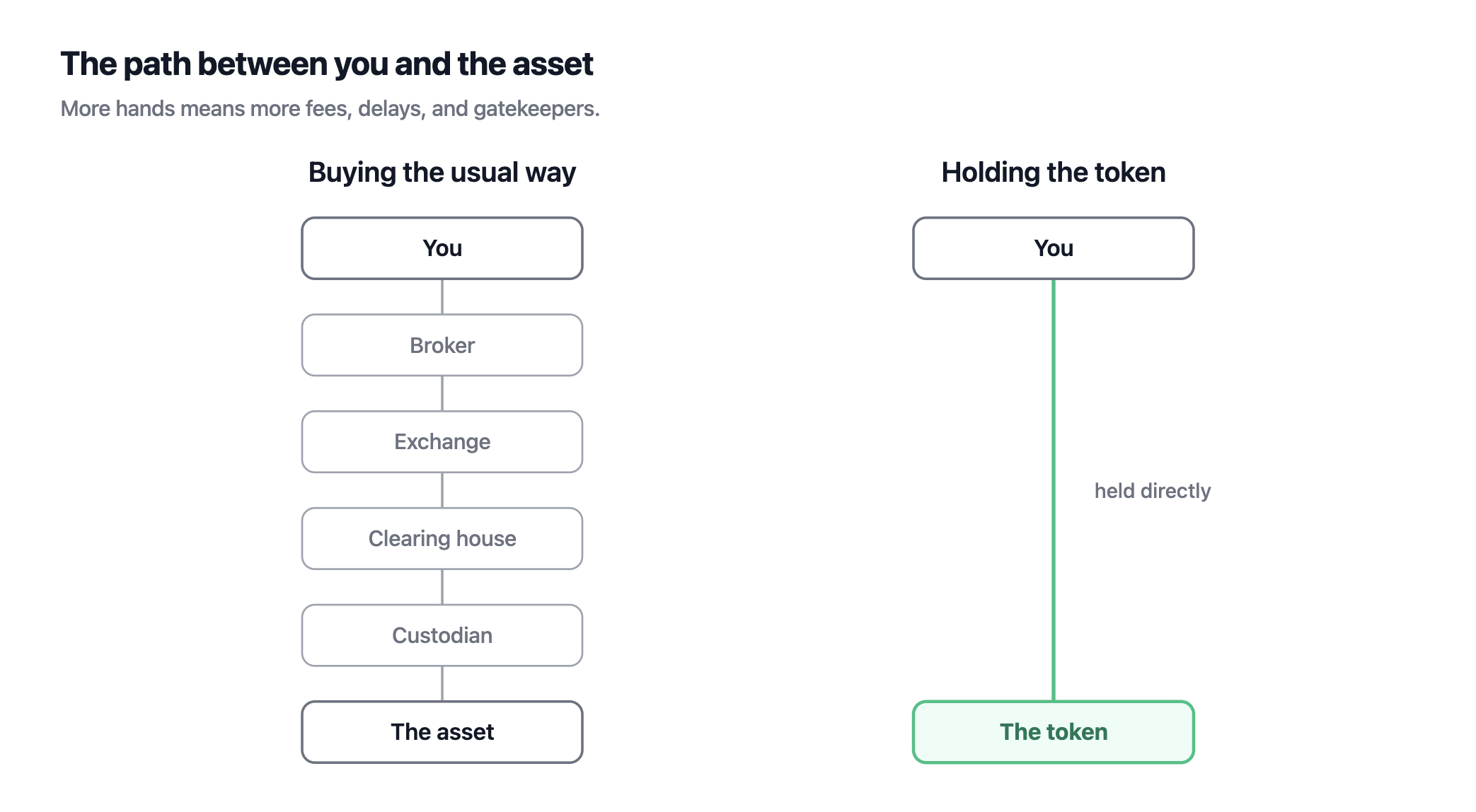

- Fewer middlemen: Holding a token directly trims the chain of brokers, exchanges, clearing houses, and custodians that a normal trade passes through.

Where it stands today

Tokenization is moving through two stages. The first is already well underway: bringing familiar assets onchain so they can be held and transferred far more freely than before. The second is where the bigger upside sits: once an asset is a token, other onchain apps can use it, not just store it. The same token might let you borrow against it (putting it up as collateral, the way a house backs a mortgage), sit inside a ready-made portfolio, or run through an automated strategy. This wider world of financial apps that run on blockchains instead of through banks is usually called DeFi, short for decentralized finance.

Most assets are still in that first stage today. Only about 5% of tokenized bonds, roughly $800 million, is actually being used inside those apps so far, and tokenized gold even less. The rest is onchain but sitting still. The pieces to connect them are arriving quickly, though, and that is where much of the next wave of growth is expected to come from. Having a token onchain is one thing, and having it actually do something onchain is the next step, which is the part most people overlook.

What to watch for

A few things to keep in mind before buying:

- Issuer risk: The token is a claim on an asset a company holds for you. If that company fails or mismanages it, your claim is only as good as the law and paperwork behind it. The issuer matters more than the technology.

- Thin trading: Most RWA activity is buying, not active trading. Large holders move in big, infrequent blocks, so selling a less-liquid token in a hurry can be hard.

- Fuzzy numbers: Figures vary depending on whether they count only freely transferable tokens or also assets locked inside one platform, so the same category can look very different from one source to the next.

How to buy RWAs

Buying an RWA does not require a brokerage account or a bank in a particular country, though it does require clearing whatever eligibility rules attach to the specific asset and to where you live. You hold them in an app or account built for tokens, fund it, and pick what you want.

An app like Glider is one place to do it. You can hold tokenized Treasuries, tokenized gold, and tokenized US stocks together in a single account. You can also buy some of these straight from the company that issues them, or through other apps and exchanges that list them. Before you buy anything, check what the rules where you live allow.

None of these assets are new. Governments have sold Treasury bills for more than a century, and gold has been a store of value for thousands of years. However, tokenization brings new reach where ownership that used to depend on where you lived and which institutions would serve you can now travel over the internet. Right now, we have a faster version of the same asset on chain, but with near term developments, we will soon see these tokens connect and start to behave like programmable money.

What does an RWA mean?

RWA stands for real-world asset: something with value in the ordinary financial world, like a bond, a company share, or gold, issued as a token on a blockchain.

What are examples of real-world assets?

The largest are tokenized US Treasuries and gold, followed by tokenized stocks, money-market funds, private credit, and dollars held as stablecoins. Treasuries and gold are the most established categories.

Are real-world assets safe?

The token is a claim on an asset a company holds for you, so the main risk is that issuer. If it fails or mismanages what backs the token, your claim is only as good as the law and paperwork behind it. This isn't investment advice.

Can anyone buy RWAs?

You don't need a brokerage account or a local bank, but whether you can hold a given RWA depends on the rules where you live and on the specific asset. Check what's allowed in your country first.

What's the difference between RWAs and stablecoins?

Stablecoins are tokenized dollars and are usually counted on their own. RWA more often refers to the other assets, like bonds, gold, and stocks, though stablecoins are technically the largest tokenized real-world asset of all.