What Is Slippage in Crypto, and When Does It Actually Matter?

You find a token you want to buy, you see a price on the screen, and you tap the button to confirm. By the time the trade goes through, the amount you received is a little less than the number you were just looking at. That small difference between the price you expected and the price you actually got is called slippage, and it is one of the most common things that confuses people when they start trading crypto. It is worth understanding, but how much it should worry you depends almost entirely on what kind of investor you are.

What slippage in crypto actually is

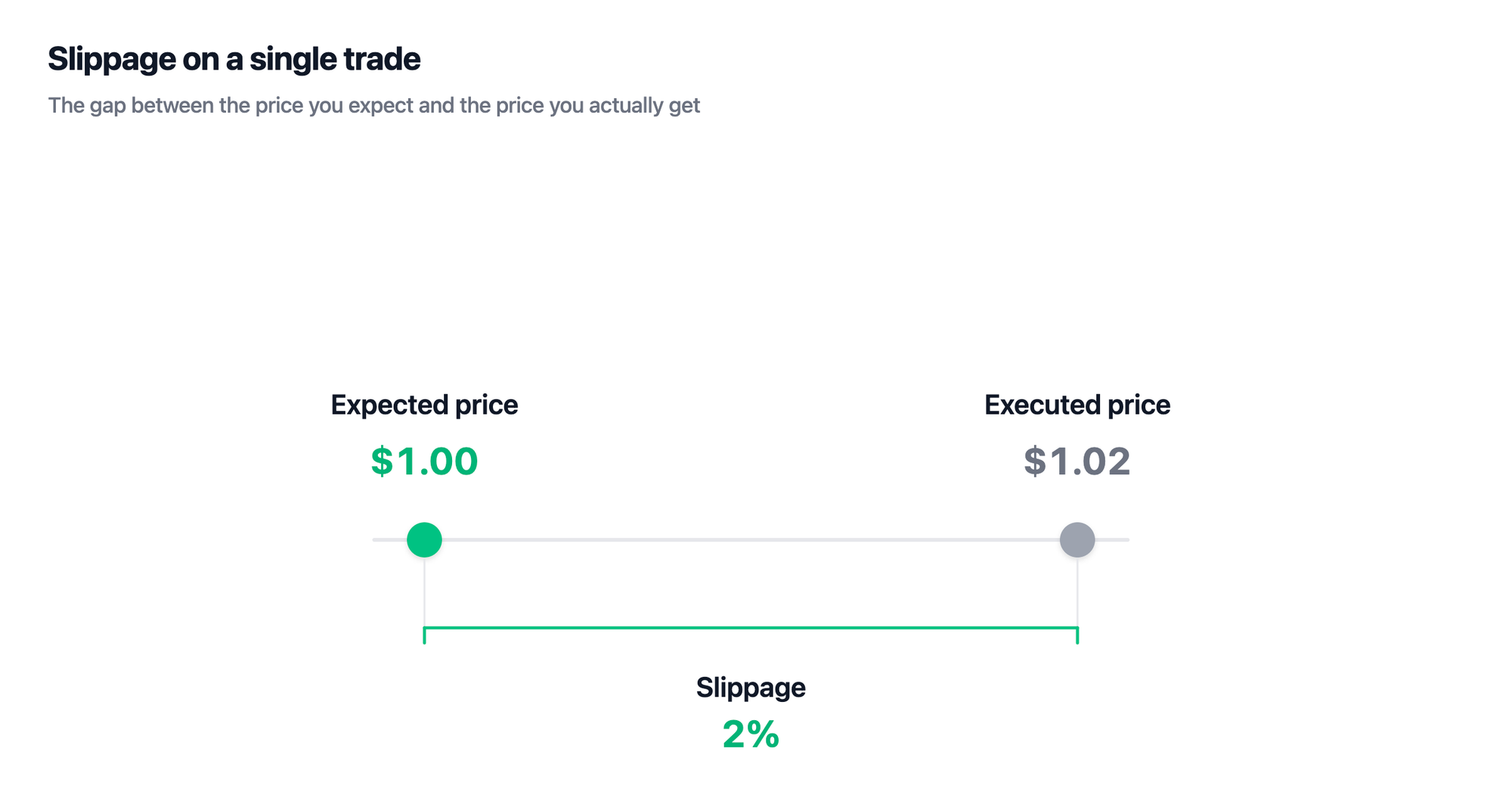

Slippage is the difference between the price you expect to pay for a trade and the price at which the trade is actually filled, usually described as a percentage of the trade size. If you expect to pay $1.00 per token and the order completes at $1.02, you have experienced 2% slippage. On a $500 order that is only a few dollars, but the same 2% on a $50,000 order is a thousand dollars that leaves your pocket without ever showing up as a fee.

It can run in either direction. Negative slippage, where you pay more or receive less than you planned, is the version people usually mean and the one they worry about. Positive slippage, where the price moves in your favor before the trade settles, also exists and quietly works to your benefit now and then. Whether either happens comes down to what is going on underneath the trade.

Why slippage happens

It helps to understand that slippage is not a glitch and it is not a hidden fee that someone is charging you. It is simply what happens when the market cannot fill your order at exactly the price you saw, and there are a few reasons that can be the case.

- Volatility. Crypto prices move quickly, and the price on your screen is really a snapshot of a moment that has already passed by the time you confirm anything. In the short window between your confirmation and the moment the trade settles, the price can move enough to change what you actually pay, which is why slippage tends to spike during sharp rallies, sudden crashes, and major news, when the price is travelling fastest.

- Thin liquidity. This is just a way of saying there are not enough buyers and sellers active in that market to match your order cleanly at one price. Liquidity is the depth of orders sitting near the current price, so a heavily traded coin like Bitcoin has plenty of people willing to buy and sell near where it trades, while a small or newly launched token might have very little waiting nearby. When that depth is shallow, your order has to reach past the best available price and take whatever sits a little further out, and that distance is where the difference comes from.

- The size of your order relative to the market. Buying a small amount of a major coin barely registers against everything else changing hands, but a large order in a small market is different, because there is not enough sitting at the current price to satisfy it. The order works its way up through progressively worse prices until it fills, and in doing so it pushes the price against itself, an effect usually called price impact. The bigger your order is compared to the market it lands in, the more of that you cause yourself.

- Network congestion. Sometimes the blockchain itself is busy and your trade has to wait its turn to be processed. While it waits, the price keeps moving in the background, so a trade that looked fine when you sent it can settle at a different number.

There is also a distinction most beginner guides skip over. On an exchange that matches individual buyers and sellers through an order book, a running list of the prices people will buy and sell at, slippage usually comes from the price moving while your order waits to be filled. On the kind of exchange that trades against a shared pool of funds instead of matching people directly, the price is set automatically by the balance of what is in the pool, so every purchase mechanically nudges it higher as it draws the asset out. The most damage tends to happen when a large order lands in a market with very little liquidity, where the order itself pushes the price against the person making it.

What slippage actually costs

The clearest illustration of that combination is a trade that happened in March 2026. Someone attempted to swap roughly $50 million of one token for another in a single transaction, on a market that came nowhere close to having enough liquidity to absorb an order that size. Because the pool it traded against was so shallow relative to the order, the price moved violently as the trade ate through what little was available, and by the time it finished the person walked away with only about $36,000. That works out to a price impact above 99% and the loss of nearly the entire amount, with most of the missing value captured by automated traders.

What makes the story useful rather than just shocking is that nothing actually broke: no hack, no bug. The platform had even shown a warning about the price impact before the trade was confirmed, and it was confirmed anyway. This was slippage in its most extreme form, produced by forcing an enormous order through a market far too thin to handle it, the same pairing described above, at a scale most people will never reach.

🚨THE BIGGEST SINGLE TRANSACTION LOSS IN DEFI? A POST-MORTEM OF HOW A USER LOST ~$50M IN ONE CLICK

— Coin Bureau (@coinbureau) March 15, 2026

Recently, a DeFi user swapped $50.4 million of aEthUSDT into just $36,000 of aEthAAVE on the Aave platform using a CoW Swap widget.

Both protocols have now released reports on… pic.twitter.com/NsbDYUUttV

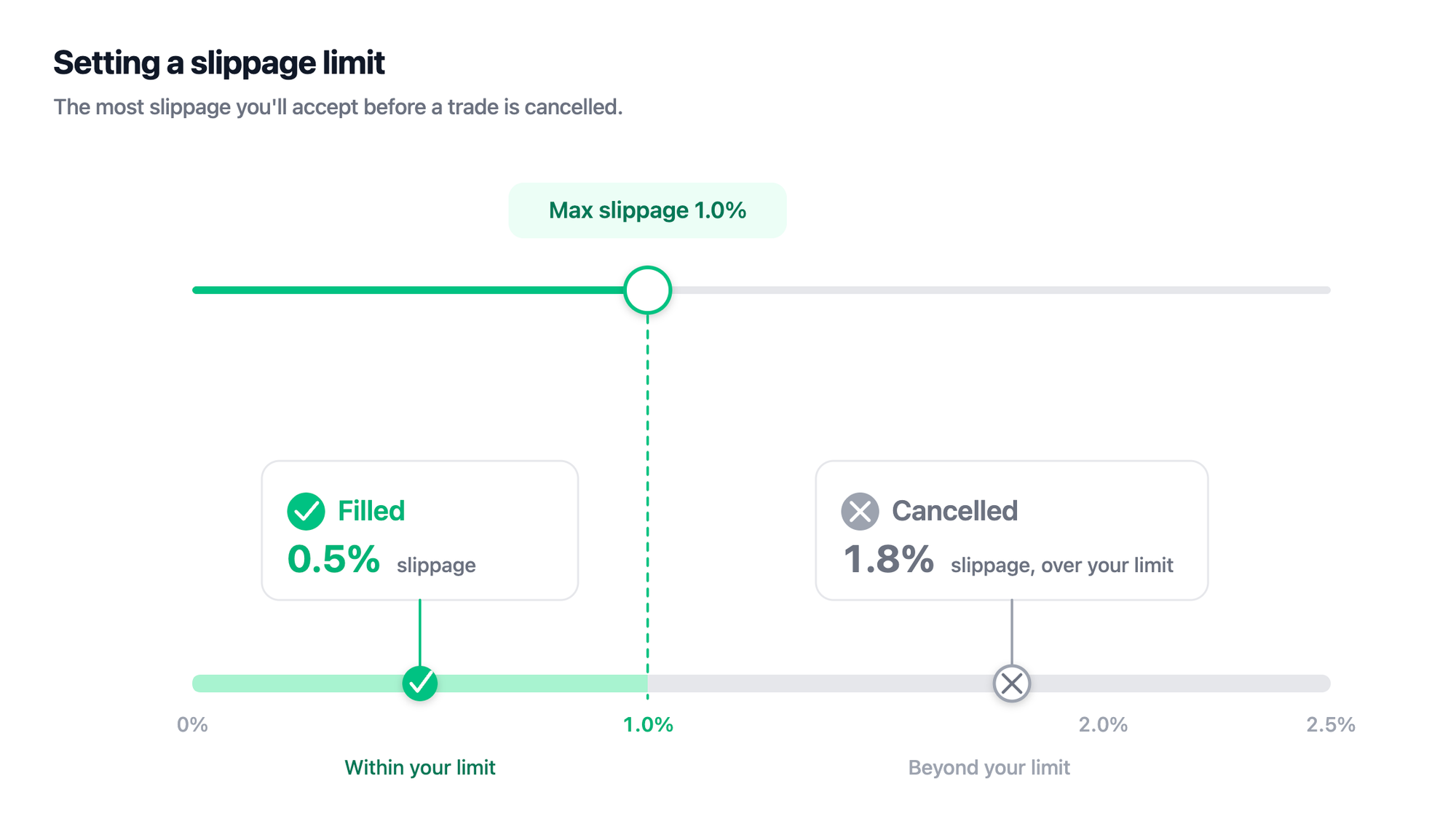

How to reduce slippage when you trade

If you are placing trades yourself, there are a handful of straightforward ways to keep slippage under control. Most exchanges let you set a slippage tolerance, a limit you choose on how far the price is allowed to move before the trade simply cancels instead of filling at a worse number than you wanted. Setting it to something like 0.5% or 1% means the trade only goes through if the price stays within that range, which protects you from the worst surprises at the cost of the occasional cancelled order. A limit order works from the other direction, letting you name the exact price you are willing to accept, with the tradeoff that the trade might never fill if the price never gets there.

Beyond those settings, the rest is about timing and size. Sticking to liquid trading pairs means there is enough depth around the current price that your order does not have to reach far to fill, trading away from launches and major news keeps you out of the windows when slippage is widest, and breaking a large order into smaller pieces stops any single trade from moving the market on its own. All of this, though, is advice for someone actively placing their own trades and watching each one fill.

When slippage stops mattering

That last point is the one that gets lost. Every tip above assumes you are the one clicking buy and sell and optimizing each fill, which describes an active trader far more than it describes most investors. If you are making occasional purchases and then holding them for years, a one-time half a percent on the way in is a minor detail against everything that happens to the price over the years that follow. The people for whom slippage compounds into a genuine problem are the ones trading in and out constantly, where it gets paid over and over, or the ones pushing oversized orders into thin markets. The advice that fills the top of the search results is written for traders, and a long-term investor mostly should not have to think about it.

Slippage is real and worth understanding, especially if you ever plan to trade actively or buy something with very little trading behind it. For most people, though, it is a smaller problem than the headlines suggest. The cases where someone loses a fortune to it are almost never bad luck, and almost always the result of reaching for a trade the market was never deep enough to absorb.

FAQ

Is slippage good or bad in crypto?

Slippage is neither, it is just a normal feature of how trading works. Most of the time it runs slightly against you, which is the negative slippage people worry about, but it can occasionally move in your favor. The amount is what matters. A fraction of a percent on a liquid token is barely worth noticing, while a large slippage figure is usually a sign that the market is too thin for the trade you are trying to make.

How do you calculate slippage?

You take the difference between the price you expected and the price the trade actually filled at, then divide that by the expected price and turn it into a percentage. If you expected to pay $1.00 and the trade filled at $1.02, the difference is two cents, which is 2% of the expected price, so your slippage was 2%.

Can you avoid slippage entirely?

Not completely, because some gap between the quoted price and the filled price is built into how markets work. You can make it very small by trading liquid assets in calm conditions, using a limit order, and keeping your order size sensible relative to the market. The cases where slippage becomes severe are almost always large orders pushed into markets too thin to handle them.