Stablecoin Yield: How to Earn on Dollars Without a Bank Account

A savings account is the most familiar way to earn a return on cash. You leave money with a bank, the bank lends it out to other people, and it pays you back a share of what it earns as interest. It's a simple arrangement, but the rate you actually get depends a lot on where you live and which bank will take you, and for plenty of people that works out to a number barely worth noticing. Stablecoins are a newer way to earn on cash that doesn't run through a bank at all, doesn't involve paperwork, and doesn't depend on which country's savings rates you happen to have access to. It's worth understanding what it actually is, where the return really comes from, and how it compares to the interest you already know.

What is a stablecoin, and what makes it "stable"

Everything here rests on what a stablecoin is, so it's worth starting there. A stablecoin is digital cash that's pegged to a real currency, so one USDC is designed to always be worth one US dollar, and one EURC one euro. It behaves more or less like the money already sitting in your account, except it lives on different infrastructure, and that's what lets it move around and earn without a bank running it.

The value holds because of what sits behind it. The most established stablecoins work a lot like a money-market fund: the company that issues the coin holds reserves, mostly cash and short-term US government debt, and every coin in circulation is effectively a claim on those reserves. That backing is the reason one USDC keeps trading at a dollar instead of slowly drifting away from it.

The names are what make this concrete rather than abstract. USDC is issued by Circle, which is a publicly listed company on a US stock exchange and operates under financial regulation, so it's about as far from anonymous internet money as a stablecoin gets. USDT, the largest one by size, is issued by Tether. Circle also issues EURC, a euro-pegged version, and that's really what makes earning on euros possible in the first place without holding a euro bank account.

Not every stablecoin is built on cash reserves, though. Some are backed by other crypto or by trading strategies instead, like Ethena's USDe, and those come with a different and generally higher set of risks, which is why the well-reserved, regulated coins are the sensible place to begin.

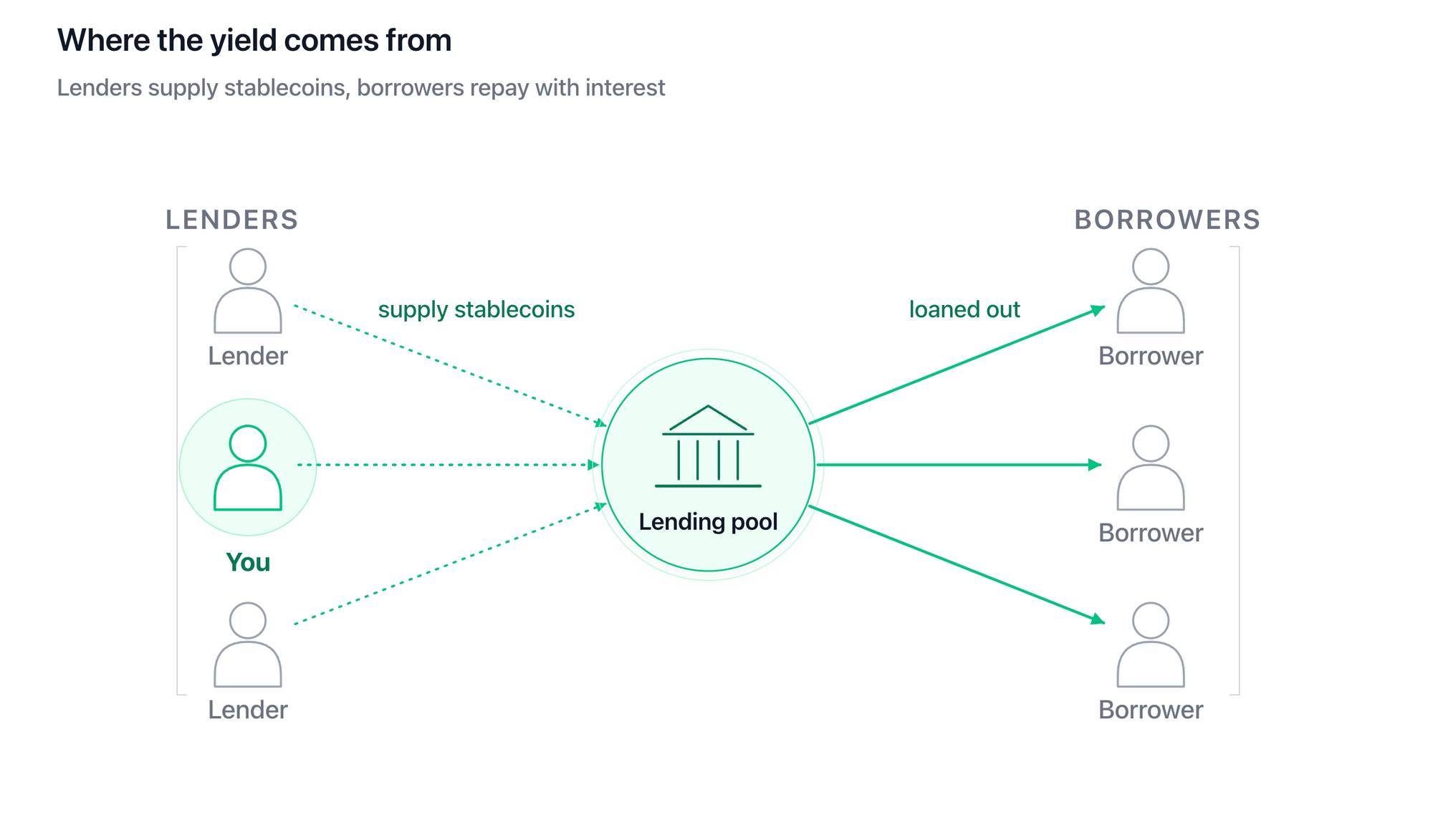

What is stablecoin yield, and where does it come from

Yield is just what you earn for letting that digital cash be put to work, which is the same basic idea as earning interest on a deposit. It isn't the issuer quietly paying you out of its own pocket, and it isn't being conjured out of nothing. When you earn stablecoin yield, your digital dollars are being lent to other people who pay interest to borrow them, which is the same mechanism a bank runs on, just with the bank taken out of the middle.

Taking the bank out is most of the reason the numbers tend to be higher, and there's nothing clever going on. A bank pays you interest because it takes your deposit, lends it out at a higher rate, and keeps most of the gap between the two for itself. Without that middle layer absorbing the difference, more of the actual lending return ends up reaching the person who put the money in. It's the same structure as a savings account underneath, with different plumbing, and that's genuinely the whole story.

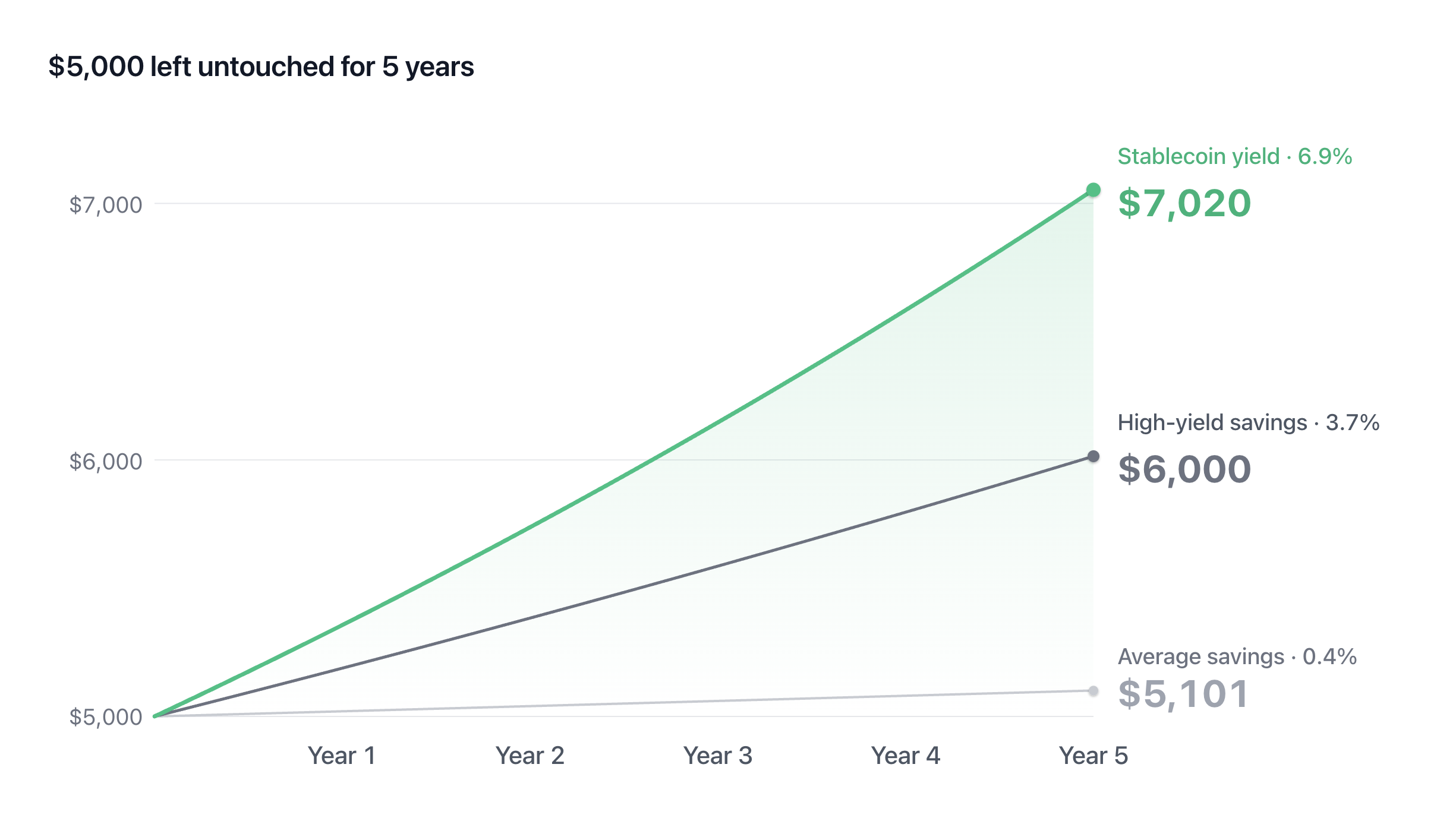

Stablecoin yield versus a savings account

A worked example makes the gap easier to see. Imagine two people who each start with $5,000 and leave it alone for five years. The first puts it in a strong high-yield savings account paying around 3.7%, while the second earns stablecoin yield at a rate closer to 6.9%. There's a third number worth keeping in mind too, which is the national-average savings rate of roughly 0.4%, because that's the line most people are actually on whether they've ever checked or not.

In the first month the difference between the three is small enough to be unconvincing. The separation is really a compounding effect, and compounding only shows what it can do given time, so it's over the five years that the three paths pull meaningfully apart. The point of the comparison isn't that one number happens to be bigger than another. It's that a strong savings rate has never been something most people could simply opt into, and earning on a different currency altogether, like holding euros through EURC, wasn't realistically on the table for an ordinary investor before stablecoins existed, whereas now it is.

How to start, and where to park cash in between

The practical version of all this is short. You hold a well-reserved stablecoin like USDC or EURC, and then you put it somewhere that earns the lending return on your behalf rather than asking you to manage it yourself.

That's where Glider fits in: it lets your stablecoins earn yield through Lending without you having to deal with any of the underlying mechanics. The part that tends to matter most for someone who's still deciding what to actually invest in is that you don't have to choose between earning and waiting, because you can park your cash there and let it keep generating yield while you're undecided, then move it into investments whenever you're ready instead of leaving it idle in the meantime.

For a long time, earning a real return on cash came down to a bank deciding to let you in, and earning on another currency came down to having an account in that currency at all. That isn't the only way it works anymore, and once you've seen the difference five years of it can make, it's a hard thing to go back to not knowing.

FAQ

Is stablecoin yield safe?

It carries real risks that a savings account does not, mainly that the platform doing the lending could run into trouble or a stablecoin could briefly trade below its peg. It is not risk-free, but using well-reserved, regulated stablecoins like USDC or EURC and established places to lend them keeps the risk much closer to the cautious end of the range.

Where does stablecoin yield actually come from?

It comes from your stablecoins being lent to other people who pay interest to borrow them, which is the same basic mechanism a bank uses. The difference is that there is no bank in the middle keeping most of the spread, so more of the lending return reaches you.

Can you lose money earning stablecoin yield?

Yes. The two main ways are a failure at the platform handling the lending, or a stablecoin losing its peg and not fully recovering. Sticking to established stablecoins and venues reduces both, but neither is impossible, which is why the higher rate exists in the first place.

Do you need a bank account to earn stablecoin yield?

No. The entire point is that it works without opening a bank account or going through a bank's approval process, and it lets you earn on dollars through USDC or euros through EURC even if you cannot easily open an account in those currencies.