What Is Dollar-Cost Averaging? A Plain Guide to the Strategy That Beats Most Investors

Every investor wants to buy low and sell high. Almost nobody manages it consistently, including the professionals who do this for a living. The cost of trying is one of the more expensive habits in personal finance. You buy something the week before it drops fifteen percent. You sell during the worst week of the year and watch the market recover without you. You sit in cash waiting for the right moment, and the right moment never quite arrives.

Dollar-cost averaging is what investors do when they accept that timing is impossible and decide to win anyway. The strategy is simple: invest a fixed amount on a fixed schedule, regardless of where the price is on any given day, and let the schedule do the work. The same amount, every month, year after year, into the same investment.

What dollar-cost averaging actually is

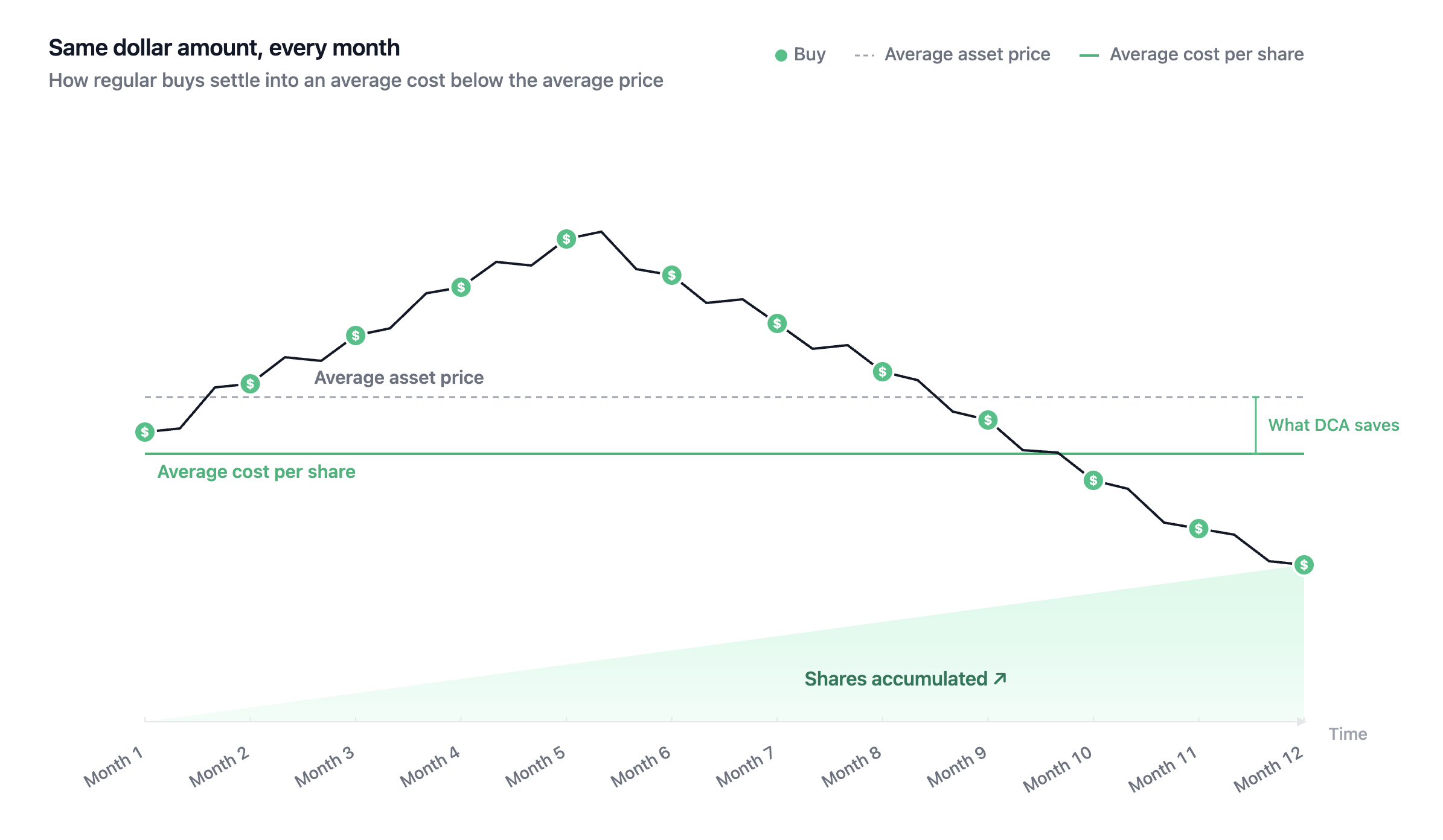

Dollar-cost averaging means putting the same dollar amount into the same investment at regular intervals. The intervals are usually monthly because that matches how most people get paid, but weekly or biweekly works the same way. The point is that the schedule does not change based on the price. When the asset is expensive, the fixed amount buys fewer shares. When the asset is cheap, the same amount buys more. Over time, the average cost ends up lower than the average price of the asset over a period of time.

Most people are already doing this without thinking of it as a strategy. Anyone with a regular contribution flowing into a retirement account or a savings plan is dollar-cost averaging by default. The payroll system is the schedule. The contribution amount is the discipline.

Why dollar-cost averaging works

The math edge is real, but it is not the main reason the strategy works. The bigger benefit is that it removes the daily decision of whether to buy today or wait. That decision is the one most retail investors get wrong, repeatedly. Markets dip and the obvious move feels like waiting. Markets rally and the obvious move feels like waiting for a pullback. Both instincts are usually wrong, and they compound over years into a portfolio that underperforms the market it was supposed to track.

Dollar-cost averaging turns investing from a series of judgment calls into a recurring habit. It is closer to a behavior shield than a math trick. Investors who stick with a schedule tend to stay invested through downturns because the schedule does not change just because the news did. That consistency, over decades, is worth more than any cost-basis advantage on any given trade.

The honest tradeoff: Vanguard's research found that lump-sum investing beats dollar-cost averaging about two-thirds of the time over long horizons, because earlier money has more time to compound. The case for dollar-cost averaging is not return optimization. It is risk smoothing. The strategy you will actually follow always beats the one that is theoretically optimal but emotionally impossible.

What dollar-cost averaging looks like over eight years

The math is one thing. Seeing it work over real time, with real prices, is another.

Picture someone who started buying $30 of Bitcoin every single day in the middle of 2018. Just $30, automatically, no decisions involved. The timing was unflattering. Bitcoin had already fallen from its 2017 peak and would keep falling toward the end of that year. Anyone trying to time the entry would have stopped buying. The schedule kept going. Through the rest of the bear market, through the crashes, through the rallies past $65,000 and $100,000 and every swing in between. Same $30, every day, for eight years.

By the time eight years had passed, the total contributed came to roughly $86,000. The position, at current prices, is worth close to a million dollars. The same person, trying to time those eight years themselves, would almost certainly have done the opposite of what the schedule did. They would have bought near the peaks because that is when buying feels obvious, and stopped buying near the bottoms because that is when buying feels insane. The schedule never had an opinion about either. It just bought. And a very similar story showed up on X:

Someone has been buying $30 worth of Bitcoin daily for the last 8 years, turning $86,000 to $1 MILLION 🤯

— Trending Bitcoin (@TrendingBitcoin) May 12, 2026

WHAT A LEGEND! pic.twitter.com/HH7ciVZLvh

The interesting part of the story is not the return. It is the cost basis. Spreading the same dollar amount over eight years of wild price movement meant the average price paid per coin was nowhere near the average price Bitcoin traded at. More dollars went in when Bitcoin was cheap and fewer when it was expensive, automatically, because the dollar amount never changed even when the price did. The investor never had to guess. The schedule did the work.

Bitcoin is the illustration here because the price movements are dramatic enough to see the mechanic clearly, but nothing about the strategy is specific to it. The same pattern plays out with index funds, individual stocks, or any asset whose price moves. Volatile assets just make the underlying logic visible faster.

How to actually start dollar-cost averaging

The strategy is simple. Setting it up well is not always simple, and the gap between "I should be doing this" and "I am doing this" is where most people stall. Three things to decide.

Decide the amount. A figure that is meaningful enough to matter but small enough to be sustainable when something unexpected happens to your monthly cashflow. A reasonable test is whether you could keep contributing the same amount for a full year without checking your bank balance first. If the answer is no, the amount is too high.

Pick the schedule. Weekly, biweekly, or monthly. Monthly is the most common because it lines up with how most people get paid. Smaller, more frequent intervals smooth out price swings slightly more, but the difference over long horizons is small. Whatever you can automate is fine.

Automate it. This is the single most important step. Manual recurring buys do not survive a busy month, a bad week, or a moment of doubt about whether to skip this one. Automation removes the decision, which is the only part of the strategy that has ever been at risk. Set it up once and let it run. The way you set this up today looks different from how it looked even five years ago, because the tools have widened considerably.

Closing

Dollar-cost averaging is what most investors should have been doing the whole time. The strategy itself has not changed in seventy-five years. What changed is the infrastructure around it. It's never late to start, especially when investing has become easier than ever before.