What is Portfolio Rebalancing and why it matters?

A portfolio you set up five years ago is no longer the portfolio you have today, even if you never touched it. Stocks, bonds, and crypto grow at different rates, and a balanced mix at the start drifts into something quite different within a year or two. Someone who built a 60/30/10 portfolio in early 2021 is now holding something with materially more equity risk and a much smaller bond cushion than they originally chose, even without making a single trade.

That gap between the portfolio you intended and the portfolio you actually have is what portfolio rebalancing is meant to close.

What is portfolio rebalancing?

Portfolio rebalancing is the process of bringing your investments back to the original mix you chose. You sell some of what has grown too large and buy more of what has grown too small, until the percentages match the targets you set at the start.

A short example. You decide your portfolio should be 60% stocks, 30% bonds, and 10% Bitcoin. Three good years for stocks later, the portfolio looks more like 75% stocks, 18% bonds, 7% Bitcoin. Rebalancing trims the stocks, tops up the bonds and Bitcoin, and gets you back to 60/30/10. The point is not to predict markets. It is to keep the risk profile you originally chose. A portfolio that drifts from 60/30 to 75/25 has quietly become a more aggressive portfolio than the one its owner agreed to hold.

Why your portfolio drifts

Different assets grow at different rates, and even simple portfolios drift quickly when one component runs hot.

The last five years are a good illustration. Between the start of 2021 and the spring of 2026, the S&P 500 returned around 130% with dividends. US investment grade bonds went sideways and lost ground in 2022. Bitcoin rose 60% in 2021, crashed 64% in 2022, then more than doubled in both 2023 and 2024. A 10% Bitcoin allocation could become 25% in a strong year and 4% after a crash, all without you placing a single trade. You did not sign up to take on more risk. The market made that decision for you.

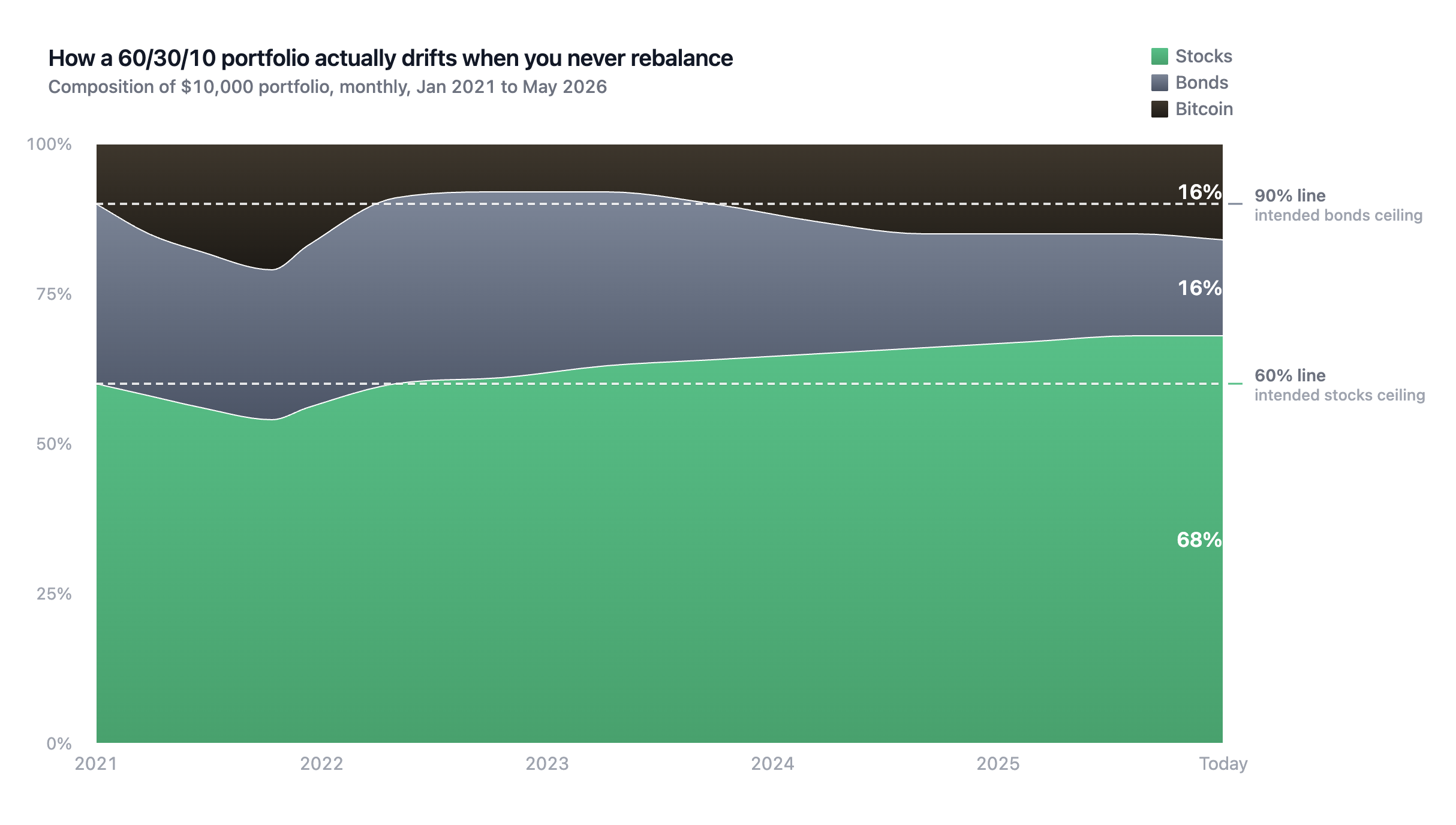

What this looks like: a real $10,000 portfolio from 2021 to today

Imagine two investors. Each puts $10,000 into the same 60/30/10 portfolio on January 1, 2021, split between the S&P 500, US investment grade bonds, and Bitcoin. The first never touches the account again. The second rebalances every December back to the original mix.

After five years, the rebalanced portfolio is worth around $19,000. The untouched portfolio is worth around $18,200. The rebalanced version is modestly ahead, mostly because the 2022 crash hit harder for the investor who entered the year overweight on Bitcoin from the 2021 run-up.

The dollar gap matters less than what the untouched portfolio has become. The investor who chose a balanced mix in 2021 is now holding something noticeably more aggressive, with roughly half the bond cushion they started with and a much larger crypto position. Rebalancing is not a reliable return booster, and in long bull runs it usually costs you. What it does reliably is keep your portfolio matched to the risk you originally chose.

How often should you rebalance?

Most rebalancing strategies fall into one of three categories.

- Calendar-based rebalancing means resetting the portfolio on a fixed schedule, usually once a year or once a quarter. Easy to remember, easy to skip.

- Threshold-based rebalancing means resetting whenever any allocation drifts more than a set distance from target, often 5 percentage points. More responsive to market moves, but requires you to keep checking.

- Hybrid rebalancing combines the two. You check on a schedule, perhaps every quarter, and rebalance only if drift exceeds the threshold. Research from Vanguard suggests this captures most of the benefit without forcing unnecessary trades.

All three depend on a human remembering to do the work, which is where they quietly fall apart in practice.

The friction of manual rebalancing

Manual rebalancing has a surprisingly high failure rate among retail investors. Plenty of people who plan to rebalance annually actually do it every two or three years, if at all.

It is not that rebalancing is hard to understand. It requires logging in, calculating drift, deciding what to sell and buy, executing trades, and accepting that you are selling things that have just gone up in value. That last part is the hardest. Selling winners feels wrong even when the math says it is the right move. Trading fees, capital gains taxes in taxable accounts, and the time it all takes add up too. The behavior gap, not the knowledge gap, is the real problem.

Automated rebalancing: the modern default

The first real answer to manual friction was the robo-advisor. Wealthfront and Betterment automated rebalancing inside traditional brokerage accounts more than a decade ago, and rebalancing on autopilot is now standard on any modern investing platform.

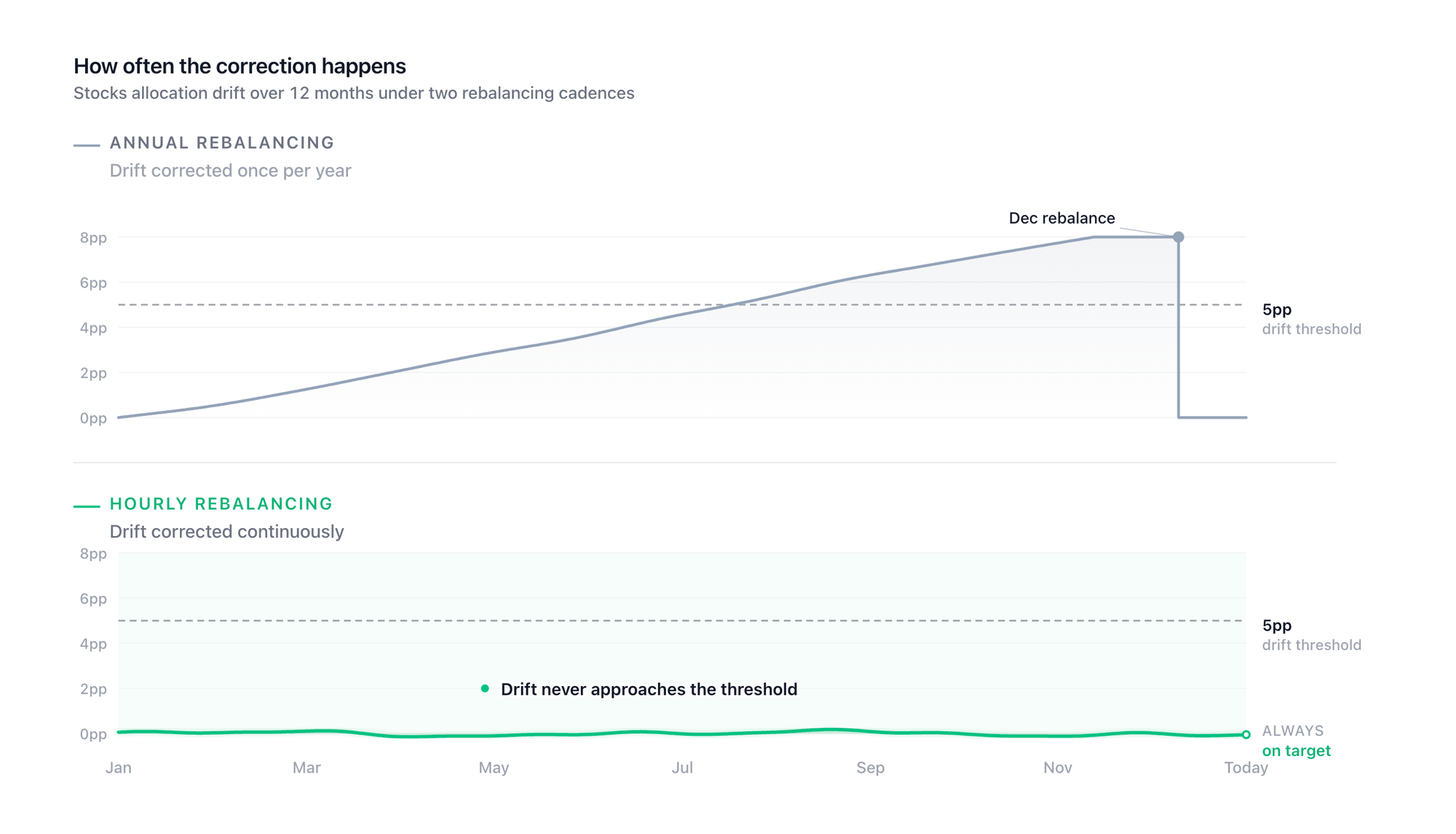

The newer answer goes further. Instead of rebalancing once a year or once a quarter, some platforms rebalance continuously, checking your allocation against your target on a fast cadence and correcting drift as soon as it appears.

The rebalanced portfolio in the backtest above assumed an investor who actually remembered to log in every December for five years straight. Hourly rebalancing removes that assumption.

Drift is constant. Markets keep moving whether you are paying attention or not, and the portfolio you set up last year is becoming something different right now. Discipline beats prediction over long horizons, but only when the discipline actually happens. The version of investing where you set the structure once and the structure stays has quietly become the default on the tools built recently.

How often should I rebalance my portfolio?

For manual rebalancing, once a year is the most common answer, and Vanguard's research suggests annual or threshold-based rebalancing captures most of the benefit without overtrading. Quarterly rebalancing is fine but tends to add cost without adding much value. Daily or weekly manual rebalancing is almost always too much. Automated platforms can rebalance more frequently because the friction and cost of each rebalance are dramatically lower.

What is the 5/25 rule for rebalancing?

The 5/25 rule is a threshold-based rebalancing trigger. You rebalance whenever any allocation drifts more than 5 percentage points from its target for major holdings, or more than 25% of its target weight for smaller holdings. So a 60% stock allocation would trigger a rebalance at 55% or 65%, and a 5% holding would trigger at 3.75% or 6.25%. It is meant to keep you from rebalancing too often on small positions while still catching meaningful drift.

Should I rebalance during a market downturn?

Usually yes, even though it feels wrong. A downturn is precisely when rebalancing is most valuable, because it forces you to buy assets that have fallen and trim assets that have held up. The hardest part is psychological, not mathematical. This is also why automated rebalancing tends to outperform manual rebalancing in volatile periods. The system does not hesitate.

Is portfolio rebalancing worth it?

For most investors, yes. The main benefit is risk control rather than higher returns. A portfolio that drifts unchecked tends to become more aggressive over time, because winning assets compound their share of the total. Rebalancing keeps the risk level you originally chose. In some periods, particularly those with sharp downturns, rebalancing also improves returns. In long bull runs, it can modestly cost you.