What Are Auto Investing Apps and How Do They Work?

Most people don't fail at investing because they pick the wrong stocks. They fail because they never start, or they start and stop. An auto investing app exists to make showing up the default. It buys the assets you've chosen on a schedule you've set, or maintains a portfolio mix without you having to do the rebalancing manually, or both. This post explains the few different shapes these apps come in, why the underlying logic works, and how to figure out which one fits.

The three flavors of auto investing apps

Automated portfolio platforms put you in control of the strategy and let the platform do the work. You pick the assets and the weightings yourself, and the platform handles execution and rebalancing. Glider, M1 Finance and Public all sit in this category in different ways. These work best when you want a say in what you hold but not the work of maintaining it.

Robo-advisors pick the portfolio for you. You answer a few questions about goals and risk tolerance, the app builds an allocation of low-cost ETFs, and you set a recurring contribution. From there it manages everything: rebalancing, sometimes tax-loss harvesting, sometimes tax-advantaged account types like IRAs. Wealthfront, Betterment, and Schwab Intelligent Portfolios are the well-known versions in the US. These work best when you want hands-off allocation and you trust the app to make the choices.

Round-up apps invest spare change from your everyday spending. You buy a coffee for $3.40, the app rounds up to $4 and invests the $0.60. Acorns and Stash are the names everyone knows. These work best when you're starting from zero and the goal is the habit, not the balance. The fees matter more than they look on small balances, but for the right person the habit matters more.

Most readers will know within a sentence which one fits them.

Why auto investing actually works

The case for automating investing is older than the apps and stronger than most of them admit. Three things make it work.

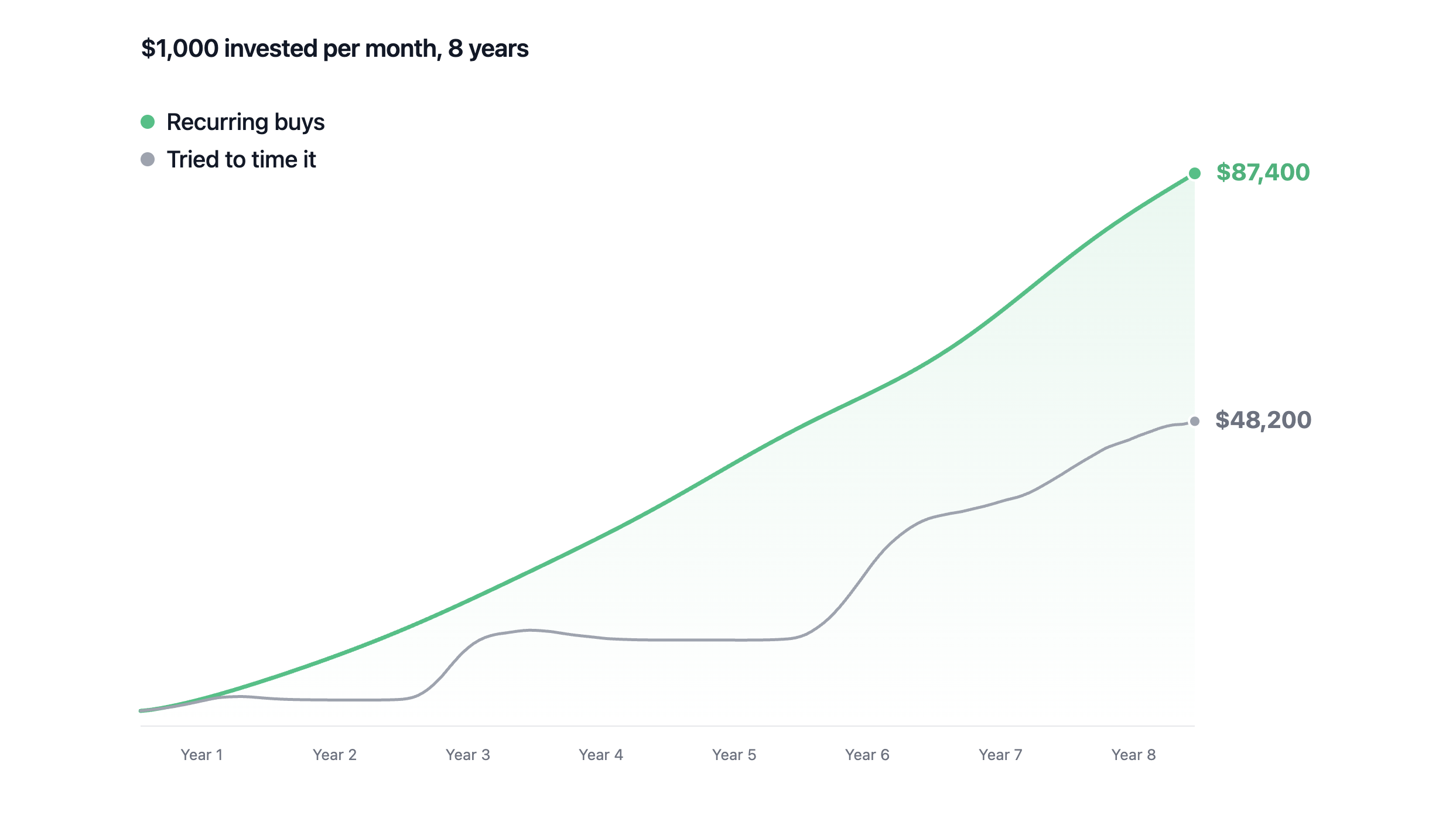

Consistency beats timing. Most retail investors who try to pick entry points lose to the ones who just keep buying. Decades of data on dollar-cost averaging back this up, and the reason is mechanical. If you're contributing the same amount every month, you buy more shares when prices are low and fewer when they're high, which lowers your average cost over time without you having to think about it.

It removes the decision. Investing on a schedule means you don't have to talk yourself into it on a bad week, and bad weeks are usually when stopping costs you the most. The investor who pauses contributions every time the market drops misses most of the recovery.

Compounding works on contributions, not just returns. The investor who puts in $200 a month for twenty years and earns market returns ends up far ahead of the one who contributes $5,000 once and waits. The recurring contribution is the engine.

What to look for when picking an auto investing app

Four questions a buyer should be able to answer about any app before signing up.

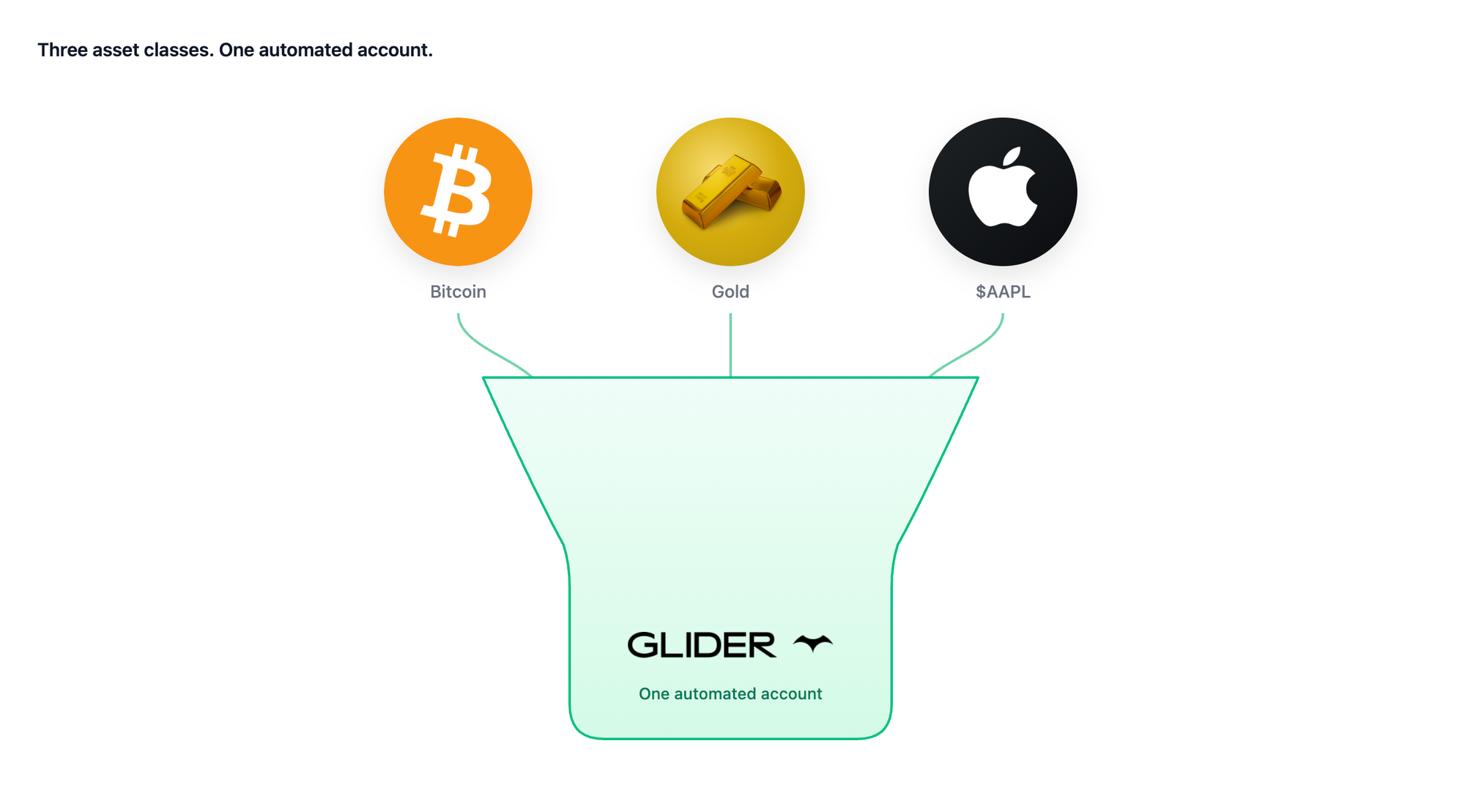

What assets can you actually hold? Some apps only offer prebuilt ETF portfolios. Some let you hold individual stocks. A newer category lets you hold tokenized stocks, gold, treasuries, and crypto in the same account. The menu shapes everything else.

What kind of automation does it support? Recurring buys mean the app buys X dollars of Y on a cadence you set. Auto-rebalancing means the app keeps your allocation on target as prices move. Some apps do one well, some do both, and the difference shows up the moment your portfolio drifts.

Where can you use it from? Local availability matters more than marketing usually admits. Most US auto investing apps don't work outside the US. Most non-US apps have a smaller asset menu than the US ones.

What does it cost? Fee structures vary. Some apps charge a flat monthly subscription, which can quietly eat returns on small balances. Others make money through spreads on trades, expense ratios on the underlying funds, or conversion fees if you're funding in a non-USD currency.

Of these four, the question of what you can actually hold is the one that's changed the most in the last year.

Auto investing across any asset, in one place

Auto investing apps were built around a fixed menu. US ETFs, US stocks, sometimes crypto on a separate app. If you wanted to auto-invest into a basket that crossed asset classes, you used three different apps and accepted that none of them talked to each other.

That's been changing. Stocks, gold, and treasuries are starting to get tokenized, which means issued as digital versions on a public network. The result is that assets that used to live in three different brokerages can now sit in the same account and be automated together.

Glider is where you actually do this. You fund an account, pick the assets and weightings you want, and the platform handles execution and rebalancing on the schedule you set. Recurring buys are supported once your account is funded, and any portfolio you build can rebalance itself automatically at the cadence you choose. The asset menu spans tokenized US stocks, ETFs, gold, treasuries, and crypto, all inside one account.

The boring path

The honest answer to "how do most people who built real wealth get there" is that they bought into something reasonable, kept buying, and didn't do much else. It's a deeply boring story and it's also the one with the highest hit rate. Auto investing apps exist because the boring path is hard to walk on willpower alone, and software is better at it than we are.

Q&A

What is an auto investing app?

An auto investing app is software that buys investments for you on a schedule you've set, or maintains a portfolio you've chosen by rebalancing it on its own. Some apps automate the contributions, some automate the allocation, and the better ones do both. The point is that the buying happens whether you remember to do it or not.

Is auto investing actually a good idea?

For most people building long-term wealth, yes. The historical data on dollar-cost averaging is consistent: investors who contribute the same amount on a recurring schedule generally outperform those who try to time the market. Auto investing isn't a strategy on its own, but it's the discipline that makes whatever strategy you've chosen actually work.

Can I auto invest in stocks, gold, and crypto in the same place?

Until recently, no. Traditional auto investing apps were built around a fixed menu of US ETFs and stocks, with crypto living on a separate app. The newer category of automated portfolio platforms, including Glider, lets you hold tokenized stocks, ETFs, gold, treasuries, and crypto inside one account and rebalance across all of them on a schedule.